Noel News

“Co-operate with the inevitable.”

DALE CARNEGIE

Welcome to our June Newsletter

What a remarkable three weeks it has been. Never has a budget received such publicity. And of course, as time passes and people analyse it more closely, some of the hidden surprises are starting to emerge. I’ll talk about that later in this newsletter. But more than ever, I think it’s important to keep your head down, stay the course and get good advice.

Over the next year many people with investment assets will be reviewing their affairs and deciding whether to bite the bullet and sell before 30 June 2027, when the CGT rules are proposed to change. But tax is only part of the equation. The bigger question is what you would do with the proceeds, and whether the asset still has strong long-term potential.

The proposed changes also make superannuation even more attractive from a tax perspective. If access before age 60 is not an issue, super may become one of the best long-term homes for investment money. Just remember that your balance each 30 June affects your ability to make future after-tax contributions. If you have owned an asset for a long time, keeping it after 30 June 2027 may still make good sense if it is a quality asset, because the capital gain is apportioned over the entire ownership period and the portion caught under the new rules may not be significant. Once again, this is an area where expert advice and careful planning could save you a fortune.

PODCAST

Making Money

Made Simple

with Noel Whittaker

Renowned broadcaster John Deeks and I discuss all the big topics covered in this newsletter in detail each month.

Listen now on Spotify

Property prices

Property is all over the newspapers since the budget, and of course the headlines are often sensational. Here’s my take.

First, there is no such thing as “the property market”. There are many property markets. Apartments in Cairns are a different market from houses in Balmain. Some markets are booming, and some are going nowhere at all. What the budget is likely to do is make existing investors more reluctant to sell. They understand the cost of replacing an investment asset, and many will be reluctant to crystallise a capital gain. If they are thinking of selling, I suspect a lot will wait until at least June next year to maximise the current CGT discount.

While writing this, I saw an interesting piece on the ABC. They interviewed a real estate agent from Melbourne who said that at last week’s auctions there were no investor buyers — all the activity came from first-home buyers. I think that’s fantastic news. But they also interviewed a woman from Sydney who bought an apartment for $800,000 last December and says it is now worth less than she paid for it. That’s not a problem, provided she is never forced to sell in the short to medium term. It does, however, show that we are now in a different phase of the property cycle.

It’s interesting how quickly the narrative has changed. Not long ago the headlines were all about soaring property prices, buyers scrambling to get into the market and fears that housing would become even less affordable. Now the focus has shifted to falling values and stories of people losing money. The front page of The Australian on 4 June featured a tradie who bought a property for $830,000 last November and then spent another $180,000 on renovations, taking his total outlay to just over $1 million. Just six months later, the property was reportedly valued at only $850,000.

I don’t see this as a major issue. Property has always been a long-term investment and six months is far too short a period to judge whether a purchase has been successful. Markets move in cycles and there will always be periods when prices surge and periods when they pull back. What concerns me more is the effect these sorts of headlines can have on confidence. Economists call it the “wealth effect”. When property and share markets are rising, people feel wealthier and more secure, so they tend to spend more freely. When newspapers are full of stories about falling property values and market weakness, people become cautious. They postpone spending decisions, hold onto their cash and wait to see what happens next. That caution can become self-reinforcing because lower spending slows economic activity, which creates even more uncertainty. One dramatic story about a property owner taking a paper loss may generate headlines, but it tells us very little about the long-term prospects for the broader property market.

Real estate agents in Brisbane tell me investors have largely stepped back from the market, which is hardly surprising given the uncertainty created by the proposed tax changes. Yet properties under $1 million remain in strong demand because first-home buyers are competing fiercely for a limited supply of affordable homes. At the other end of the market, the picture is quite different. Agents report that properties priced between about $1.5 million and $4 million have become much harder to sell, with prices in some areas falling by around 10 per cent as buyers become more cautious and take longer to make decisions.

| Despite what some headlines suggest, we still have a construction crisis. Apprentice numbers are at record lows, which means ongoing pressure on the building industry for years to come. Everywhere I travel in Australia I see cranes, construction sites and new developments under way. New homes and apartments cannot be produced without skilled labour, and labour shortages inevitably drive costs higher. Developers cannot continue selling properties below the cost of construction, so over time prices must reflect the true cost of bringing new housing stock to market. If prices soften further, many owners who were thinking about selling may simply stay put and wait for better conditions rather than accept a lower price, which in turn reduces the supply of properties available for sale.

There is no doubt there will be continuing pressure on rents. The budget has made property investment a less attractive proposition for many people. At the same time, population growth continues. If more people arrive and rental housing is not available, the inevitable result is greater competition for the homes that do exist. The people I worry about most are potential first-home buyers. They face the double challenge of high prices and rising rents, making it harder than ever to save a deposit and get a foothold in the market. |

|

|

Minimum wage up

Last Tuesday, the national minimum wage was increased by 6 per cent, rising from $948 a week to $1,004.90 a week, or $26.44 an hour. Workers will certainly welcome the increase, but the headlines missed an important point. The increase amounts to about $57 a week. However, around $8 of that disappears in income tax, leaving the employee with about $49 a week extra in take-home pay. Meanwhile, the employer has to fund not only the wage increase but also compulsory superannuation and other on-costs. By the time these are added up, the increase can cost the employer about $65 a week.

It’s a good illustration of how the numbers work in the real world. The employee receives an extra $49 a week in their pocket, but it costs the employer about $65 a week to provide it. Given the hospitality industry is one of the largest employers of low-paid workers, there will inevitably be consequences. Some businesses will put up prices. Others may reduce staff hours or delay hiring. Higher prices also add to inflation, which makes it harder for the Reserve Bank to justify cutting interest rates and could keep rates higher for longer than would otherwise be the case.

But the impact doesn’t stop there. Every supplier to those businesses is facing the same increase in labour costs. The bakery, the food wholesaler, the cleaning company, the laundry and the transport operator all have higher wage bills to absorb. Those costs eventually flow through the system, creating further pressure on prices. That’s why a wage increase that looks straightforward on paper can have much wider consequences throughout the economy.

Capital Gains Tax

Today I’m going to give you a refresher course on how capital gains tax (CGT) works. Understanding it could save you heaps. Sadly, despite it involving one of the largest amounts of money you could pay in your lifetime, most people don’t understand how the CGT system works.

CGT is the tax you pay when you sell an investment asset, such as property or shares, that has gone up in value since you bought it. It’s important to get expert advice, because the dates are critical. Under existing law, your profit (which is your taxable capital gain) is halved — that’s the 50% discount — provided you have held the asset for at least a year and a day. And the relevant date for CGT calculations is the sale contract date, not the date of settlement.

There is currently no special rate of tax on capital gains. The taxable capital gain, after adjustment for the discount, is simply added to your taxable income in the year the contract was signed. How much tax you pay then depends on what the rest of your taxable income is. That’s why this column is timely, given we’re now only about a month away from 30 June.

One way to reduce CGT is to time the sale for a year when your taxable income is likely to be lower. A common example is selling an investment property in the year after you retire. Another strategy is to make tax-deductible superannuation contributions, including catch-up concessional contributions where available.

CASE STUDY

Jack and Jill are in their early 70s and do not receive the age pension because the investment property they own is worth $1.2 million, which takes them over the assets test cut-off. Jack has $700,000 in super and Jill has $200,000 in super. Given their ages and the latest kerfuffle about CGT changes, they consider biting the bullet and selling the property now. Their only concern is CGT.

But they get a pleasant surprise when their financial adviser tells them they may be eligible to make tax-deductible catch-up superannuation contributions. These are contributions designed to compensate people for concessional contributions that their employer, or they themselves, did not make in previous years. Neither has made any deductible contributions since retiring at 65, so each may be eligible to make tax-deductible contributions of up to $175,000 in the next financial year. This is made up of $142,500 in catch-up contributions, plus $32,500, which is the standard concessional contribution cap for next financial year.

There are two important criteria that Jack and Jill must meet. Their total superannuation balance at the previous 30 June must be under $500,000, and they must be able to pass the work test to make deductible contributions between ages 67 and 75. This involves working 40 hours in 30 consecutive days in the financial year they make the contribution.

This is where the planning and advice come in. On their adviser’s advice, Jack withdraws $250,000 from his super before 30 June 2026 and contributes it to his wife’s super as a non-concessional contribution. Neither the withdrawal nor the deposit has any tax implications. As a result, their superannuation balances at 30 June become $450,000 each. They have now passed the first test.

Some people get a bit shy about the work test. But Jack and Jill are from the vintage where people are used to coping and making the best of what they have. Both feel there would be no trouble at all getting some sort of part-time work to qualify, given the size of the sum involved. They could get some work through Grey Army, drive for Uber or work at Bunnings.

Let’s do the calculations. The property cost $500,000, which means the capital gain will be around $700,000 if they achieve close to $1.2 million for it. They qualify for the 50% CGT discount, which reduces the taxable capital gain to $350,000. That means $175,000 will be added to the taxable income of each of them in the year the contract is signed.

They then make tax-deductible superannuation contributions of up to $175,000 each, which is taxed at 15% within their super funds. Their taxable income drops to zero and the CGT liability effectively disappears. All they need to do now is give notice to their super fund that they intend to claim a tax deduction for the contributions. Their adviser will help them with the fine-tuning, because there is no point making a tax deduction that takes taxable income below $18,200, where the zero-tax threshold ends. The purpose of this example is to show you what is possible, and the importance of getting advice and planning early.

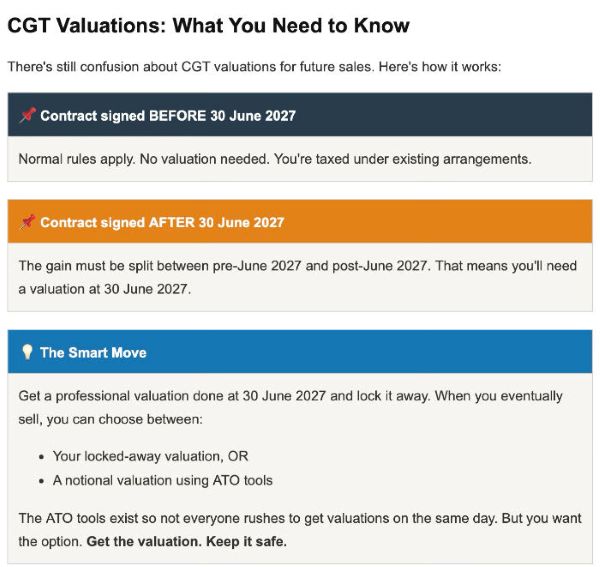

The table below is your guide to CGT valuations. Just keep in mind that if you do not obtain a valuation for assets you intend to hold beyond 30 June 2027, the ATO will determine a notional value as at that date using its ATO Tools calculator. That valuation may or may not produce the outcome you would prefer. By obtaining your own valuation as at 30 June 2027, you will have the option of using whichever valuation method delivers the better result.

The irony for mankind is that a computer program asks a human to prove that they’re not a robot.

Making Money Made Simple

The classic that started it all — now fully updated for 2026

Making Money Made Simple sold over 2 million copies in print and created billions in wealth for its readers. People still write to me saying, “If only I’d read this 30 years ago,” and “Why don’t they teach this in schools?” That’s the point: timeless principles, plain language, and a practical plan to act on today.Four decades after it first set Australian sales records, Making Money Made Simple is back in a brand-new 26th edition. This update continues to strip away the jargon and show you, step by step, how a few simple disciplines can free you from a lifetime of financial stress. This edition has been revised cover to cover, with every figure, table and rule brought right up to date.

There’s also a brand-new chapter on first home buyer incentives, and the property and investment tables have been refreshed right through to December 2025. Naturally, there’s the latest on tax, super and the housing marketAll the big recent changes have been worked in. The income tax tables now reflect the rates that apply from 1 July 2025 — including the new 16% bottom rate and the revised $135,000 and $190,000 thresholds — so the examples match what you’ll actually pay. The superannuation chapters carry the higher contribution caps, the move to a 12% super guarantee, and the latest total-balance limits.

Simple steps that genuinely change lives

Beneath the updated numbers, the heart of the book is unchanged. From getting out of debt and saving on your mortgage to investing in shares safely and turbocharging your super. Grab the updated 26th edition and start your own journey to financial independence – or give it to someone just starting their journey.

Click here to purchase Making Money Made Simple 26th Ed:

The aged care conundrum

Economics often comes down to one brutally simple principle: supply and demand. When demand exceeds supply, prices rise, queues form and shortages emerge. We see it in housing, childcare and electricity. Now we are watching the same slow-motion train wreck unfold in aged care.

|

Image by DC Studio on Freepik |

|

Australia’s oldest baby boomers turn 80 this year. For the next decade, about 80,000 Australians will turn 80 every year. That matters because the need for health and aged care services explodes in our late seventies and eighties. More people need home care. More need help with meals, transport and medication. More will eventually require residential aged care. None of this is a surprise. Governments have known this wave was coming for decades, yet Australia still rations aged care services while pretending the system is coping.

On paper, the Budget announcements sound reassuring. The government says it is delivering 32,000 additional Support at Home places in the coming financial year, on top of 83,000 places by the end of this financial year. That would bring the total number of Australians receiving support to 420,000 by 30 June 2027. To the casual observer, those numbers sound enormous.

But today around 200,000 older Australians are already waiting for home care services. These are not future applicants. These are people who have been assessed as needing care right now, or who are awaiting assessment. Some are waiting for basic domestic help. Others need assistance with showering, dressing or medication. The average wait is close to a year. In the meantime, families are left to carry the burden while juggling work, finances and their own health problems.

A recent call to an ABC talkback program says it all. The caller’s father had been stuck in a hospital bed for weeks. After battling through mountains of paperwork, the caller finally got the news she had been praying for — he had been approved for residential aged care. She was ecstatic. Then came the crushing blow: “Yes, his need for care is approved, but there are no places. It may be nine months or more before we can admit him.” That neatly sums up the crisis. Even if 420,000 Australians are receiving Support at Home services by 30 June 2027, Treasury figures suggest there could still be 37,000 people waiting — unless packages are freed up because recipients either move into residential care or die. And the demographic wave keeps growing. About 80,000 Australians turn 80 every year. Even if only half need support — probably optimistic — by 30 June 2027 we could still have 117,000 Australians needing care and waiting for it. The arithmetic is merciless. Demand is growing far faster than supply. |

When governments ration services in a market where demand exceeds supply, queues are inevitable. That is exactly what is happening in aged care. Waiting times for residential care are now around a year as well. Families and friends are forced to fill the gaps. Hospital beds are clogged with older patients who cannot safely return home but cannot access aged care either.

Last year the government lifted the market price cap for aged care accommodation from $550,000 to $750,000 so providers could build new facilities and modernise old ones. But it did not equally increase funding for financially disadvantaged residents. Providers could effectively receive accommodation funding based on $750,000 from wealthier residents, while support for low-means residents was closer to $300,000. For many providers, especially not-for-profits, the economics quickly became ugly. Some openly warned they could not continue taking large numbers of financially disadvantaged residents because the funding gap was simply too large.

The Budget throws money at the problem—increasing the accommodation supplement for homes with high numbers of low-means residents. Some homes may eventually get support equivalent to about $580,000. But here’s the rub: the extra funding doesn’t start until March 2028. And even then? It still falls $170,000 short of the indexed $750,000 market cap.

Too little. Too late. Problem not solved.

Governments are trying to walk a political tightrope. Taxpayers want quality care for older Australians, but they also want lower taxes and affordable budgets. Politicians therefore ration services while reassuring voters that everything is under control. But rationing never removes demand. It simply shifts the burden elsewhere. Families provide unpaid care. Older Australians pay privately while waiting for support. Hospitals become overflow accommodation. State governments wear the cost through longer hospital stays and rising health spending.

If aged care is rationed, surely priority should go to those with the fewest other options. The government will be asking why should millionaires receive subsidised home care when many older Australians cannot afford to buy private care and are stuck waiting for support? Residential aged care is already enormously expensive, particularly for people with high clinical needs, and those costs will keep climbing as the population ages. If governments continue to limit the number of places, tighter means testing may eventually become unavoidable.

This challenge will dominate for at least the next 20 years. But there is another issue almost nobody wants to discuss. What happens after the baby boomers pass through the system? Demographics are cyclical. Eventually demand will fall, and it may fall sharply. If governments and providers build tens of thousands of extra aged care beds now, what happens when occupancy rates decline decades from today? Providers are being asked to invest billions into facilities that may face completely different demand dynamics in 20 or 30 years’ time.

Economics always comes back to supply and demand. Australia’s aged care crisis is not happening because we failed to predict demand. It is happening because we predicted it perfectly — and still chose to ration supply.

And finally

Children are quick

Teachers ask the questions. Children provide the answers.

Sometimes the children win.

Image by Freepik

Teacher: Why are you late?

Student: Class started before I got here.

Teacher: Maria, go to the map and find North America.

Maria: Here it is.

Teacher: Correct. Now class, who discovered America?

Class: Maria.

Teacher: John, why are you doing your multiplication on the floor?

John: You told me to do it without using tables.

Teacher: Glenn, how do you spell crocodile?

Glenn: K-R-O-K-O-D-I-A-L.

Teacher: No, that’s wrong.

Glenn: Maybe it is wrong, but you asked me how I spell it.

Teacher: Donald, what is the chemical formula for water?

Donald: H I J K L M N O.

Teacher: What are you talking about?

Donald: Yesterday you said it’s H to O.

Teacher: Winnie, name one important thing we have today that we didn’t have ten years ago.

Winnie: Me!

Teacher: Glen, why do you always get so dirty?

Glen: Well, I’m a lot closer to the ground than you are.

Teacher: Millie, give me a sentence starting with “I”.

Millie: I is…

Teacher: No, Millie. Always say, “I am.”

Millie: All right. I am the ninth letter of the alphabet.

Teacher: George Washington not only chopped down his father’s cherry tree, but also admitted it. Now, Louie, do you know why his father didn’t punish him?

Louie: Because George still had the axe in his hand.

Teacher: Simon, tell me frankly, do you say prayers before eating?

Simon: No sir, I don’t have to. My mum is a good cook.

Teacher: Clyde, your composition on “My Dog” is exactly the same as your brother’s. Did you copy his?

Clyde: No, sir. It’s the same dog.

Teacher: Harold, what do you call a person who keeps on talking when people are no longer interested?

Harold: A teacher.

A big thank you to all you good people who read my newsletter.

If you were forwarded this newsletter by a friend and you would like to subscribe, you can do so here:

You can also find the subscription box in the footer of all website pages.

For more Noel News:

Download recent Noel News as a PDF

|

|