Noel News

“You are in the right place at the perfect time.

Keep enjoying the pursuit of your potential.”

DAVID MELTZER

Welcome to another newsletter

As usual we have much to cover.

We are getting close to 30 June, so if you are making superannuation contributions keep in mind they must be received by the fund before midnight on 30 June.

Furthermore, if you intend to make tax-deductible contributions to reduce a capital gain, or are considering selling loss-making assets for the same purpose, the transaction must be done before 30 June. For capital gains tax purposes the relevant date is the date of the contract was signed not the date of settlement.

Telstra

Now for the next chapter in my Telstra saga. As I explained in my last newsletter, I reported Telstra to the Telecommunications Ombudsman, which very quickly resulted in an apology from Telstra and a promise to refund my money and cancel their direct debit.

To my horror, despite Telstra’s promises, the money was not refunded, and the direct debit kept on debiting my account. I complained once again to the ombudsman. Next day, a lovely woman from Telstra in Melbourne rang me to tell me she was on the case and the money would be refunded, and the direct debit stopped, once she got “approval from the Philippines.”

I was gobsmacked that a huge Australian company can’t refund $150 without approval from another country. She rang me back four days later to say her superiors in the Philippines had instructed the money be paid by cheque and not by direct deposit. This is the 21st century! Anyway, all has ended well – the cheque arrived yesterday. Now have to go to the bank and bank the first check I’ve banked in about a year.

Minimum Pension Drawdown Rates

The government recently announced, without prior warning, that the reduction by 50% of minimum withdrawal requirements that was instituted last year due to Covid would be extended for one more year. This knee-jerk action by the government has caused a huge amount of work for both superannuation funds and financial planners.

The super funds will now need to contact all their pension fund clients informing them of the unexpected change in the requirements, and financial planners I speak to are most unhappy because over the last three months they been busily working with their clients on appropriate strategies to use next financial year when pension payments from account based pensions were supposed to be doubled. This is now all back to the drawing board.

It just seems the government can’t stop tinkering with the superannuation rules. I think we can safely say that from 1 July 2022 the normal minimum drawdown rates should apply, and unless you have more than $1.7 million in super you may also be able to contribute any surplus drawdown money up to age 75 as a non-concessional contribution without passing the work test. This assumes the legislation announced in the May budget will be passed which is highly likely.

Interesting New Product

The government’s recent Retirement Income Review pointed out that many retirees live on just the income from their superannuation, rather than drawing down on the balance as they progress through retirement. This seems to be partly due to the major misunderstanding that this is how the system is supposed to work, and partly because they don’t know how long they will live, and are so afraid of running out of money that they draw only the minimum pension required. As a result, many retirees die with a major chunk of their financial assets unspent, sacrificing their own standard of living, and leaving more to their beneficiaries.

In December 2016, Treasury called on income stream providers to develop products that would solve this problem, but to date, the industry has been slow to take up the challenge. After a lot of talk and not much action, we finally have one fund that has come up with an interesting solution.

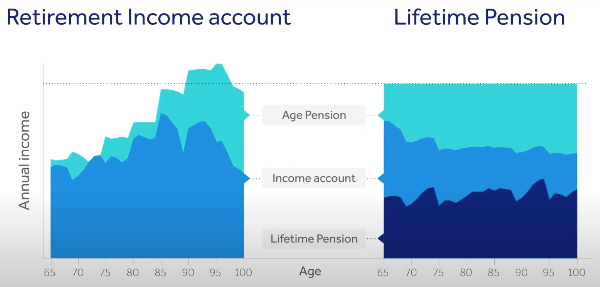

QSuper, one of Australia’s largest superannuation funds, has launched a new product, the Lifetime Pension (view their information page here), which pays a fortnightly income for life. It is designed to ensure you or your estate get back at least your initial investment, irrespective of how long you live. Ideally you would receive your return by income, but for a premature death it may be by death benefit. For example, if you invest $100,000 and die after receiving $60,000 in income, your beneficiaries will receive the final $40,000.

You can open a Lifetime Pension with your super any time between your 60th and 80th birthdays. Annual rates of income per $100,000 invested range from $6,164 to $10,834 for singles – a bit less if you take the option to cover your spouse’s life too.

These pension rates are quite a bit higher than a lifetime annuity or an account-based pension drawn at the minimum. The reason is simple: the money is pooled and invested in a balanced growth option. Apart from the fund’s low management fees and the cost of insuring the money-back death benefit, all of the money is spent on income. However, that also points to the products three drawbacks. First, this isn’t a product where you can withdraw lump sums or exit after a six-month cooling off period – you are permanently purchasing an income stream. Second, after you’ve received your purchase price as income, no death benefit is payable. And third, unlike a traditional annuity which pays fixed income for life, this product pays variable income for life.

Every 1st of July, the previous year’s income is adjusted based on how the pool performed against a benchmark net return of 5%. Simplistically, if the return is over 5%, expect a proportional pay-rise next year, but when returns are less than 5% expect a pay-cut. For example, let’s assume you were receiving $1,000 a fortnight. If net returns were 7% (2% over the benchmark), you’d expect your income to increase approximately 2% the following year to $1,020 a fortnight, but if net returns were 3% you could expect a cut to $980. In this way, the pool never runs out of money – incomes are expected generally to rise over time, helping with inflation.

A major benefit of this Lifetime Pension product is that only 60% of the sum invested is assessed for the assets test (and after you pass your official life expectancy it drops to 30%). This therefore gives assets-tested pensioners an immediate rise in their age pension, in addition to the income from the product. Also, it may allow people who are currently unable to get the age pension because they are over the assets test by a small margin to qualify for at least a part pension.

CASE STUDY

A 70-year-old couple have $600,000 in an account-based pension and $100,000 in personal assets. They draw the minimum pension, and currently receive $30,000 a year from their account-based pension and $13,960 from the age pension, as a combined income. If they invested $300,000 in a Lifetime Pension that would pay them an income of $20,053 a year, paid fortnightly, and their age pension would rise to $23,228 a year. That’s a great return on a $300,000 investment! Combined with their account-based pension income of $15,000, their total income has risen to $58,281 – an increase of $14,321 or 33%!

The Lifetime Pension product may not be suitable for income-tested pensioners because 60% of the income is assessed for the income test – this is a much higher proportion than people who are subject to deeming.

Personally, I wouldn’t recommend anyone put all their money into a product like this, as it provides no flexibility to withdraw lump sums when needed. However, it is well worth considering in conjunction with an account-based pension, as the combination would offer a very good income for life and the concessional assets test on one hand, and flexibility on the other. It’s really a matter of discussing the product with your adviser and deciding whether it’s appropriate for your own situation.

A Tax Free Portfolio

A reader wrote as follows:

“I read somewhere that a couple fully invested in Australian shares with a portfolio of around $3.5 million could potentially earn $220,000 a year and pay no tax thanks to franking credits. Is this correct or have I misunderstood it.”

Let’s do some simplistic assumptions. To keep it simple we’ll say the portfolio yields 4% per annum income and 4% capital growth. The income would be $140,000 a year and, if it’s mainly franked, would include $50,000 of franking credits. This would produce an income of $190,000 a year taxable which would be split 50-50 as they investors are a couple.

This means $95,000 a year would added to each taxable income, but they would each receive $25,000 of franking credits. If you go to the tax calculator on my website you can see that the tax on a total income of $95,000 a year would be around $22,000. The franking credits of $25,000 would eliminate all the tax and give the investor $3000 franking credit refund.

Keep in mind that as well as the income the portfolio has produced capital growth of $140,000 a year as well ,on which no capital gains tax is payable until the shares are realised. Summing up, a $3.5 million portfolio of dividend paying Australian shares should return a total tax free return of around $280,000 a year. That sure beats leaving your money in the bank.

Our First Ever Sale

I’m not really into sales because I keep the prices of my books as low as possible so everybody can benefit from the knowledge in them irrespective of their financial position. However, I have two books which will not be reprinted, and the deal of a lifetime for those who want them.

The first is my book 25 Years of Whitt & Wisdom which was designed to be my legacy book. It is a hard cover 450 page very attractive book in high-quality paper. The book is really a summary of my columns from 1987 to 2015. Given the book does not have columns past 2015, it is reaching a stage where it needs to be updated or put out to pasture. Given the extremely high costs of producing this work – it’s more like a coffee table book – it won’t be repeated. It’s not just a wonderful history of the 25 years when the Australian financial services industry was coming-of-age, it also contains a wealth of timeless value. It is still one of my favourite books and a great book to browse through.

There are only 600 copies left in stock, so I’m dropping the price to $24.95 just to clear the decks. Highly recommended.

The other is the international bestselling book written by my son James Whittaker that accompanied the film Think and Grow Rich: The Legacy, which we launched in Los Angeles in 2018. This book is a timeless classic. Not only does it introduce the original Think and Grow Rich principles in a modern context, it also includes firsthand accounts of how some of the most successful leaders on the planet today used those principles to achieve massive success. If you want a blueprint to growth, and the inspiration to make it happen, I can’t recommend it highly enough. The book has now been translated into six languages and continues to receive rave reviews.

This is the hardcover version, which has a retail price of $47.99 but Amazon have it marked down to $36.96 right now. James had a series of speeches scheduled in Australia but, due to covid, James has not been back to Australia for 18+ months, and is unlikely to return in the near future. We have a limited supply of 250 copies left, which we’re reducing to $24.95.

These are both hardcover high-quality books and postage is expensive. However, if you buy both books for $49.99 you will get free postage. This deal is first come first served.

Health Matters

Our health is a greatest asset and I’m always looking for ways to improve my knowledge in this field.

Harvard Health Publications produces some great material and you can subscribe to their weekly newsletter HealthBeat at no cost. Be warned, they are always trying to sell you an e-book, but if you see one of their publications that takes your fancy you can download the e-book for just $18.

Even if you don’t download the e-book there is still plenty of good stuff in their newsletter. Over the last year I have downloaded Controlling Blood Pressure, Strength and power training for all ages, 35 Stretching exercises to improve flexibility, and Gentle core exercises. Well worth the $18 each.

It’s a highly reputable organisation and the material was great to follow.

Click here for their newsletter archive.

From The Mailbox

I just want to give you a big thank you for your latest book Retirement Made Simple. Reading your book had taught me a lot and help me to clarify many things. I also love all your calculators. Thank you so much for providing such a comprehensive and important overview in one book. I will treasure it and refer to regularly.

Martha

And finally…

This was sent to me by one of my readers – I thought it was worth sharing.

An economics professor at a local college made a statement that he had never failed a single student before, but had recently failed an entire class. That class had insisted that socialism worked and that no one would be poor and no one would be rich, a great equalizer.

The professor then said, “OK, we will have an experiment in this class on this plan”. All grades will be averaged and everyone will receive the same grade so no one will fail and no one will receive an A… (Substituting grades for dollars – something closer to home and more readily understood by all).

After the first test, the grades were averaged and everyone got a B. The students who studied hard were upset and the students who studied little were happy. As the second test rolled around, the students who studied little had studied even less and the ones who studied hard decided they wanted a free ride too so they studied little.

The second test average was a D! No one was happy.

When the 3rd test rolled around, the average was an F.

As the tests proceeded, the scores never increased as bickering, blame and name-calling all resulted in hard feelings and no one would study for the benefit of anyone else.

To their great surprise, ALL FAILED and the professor told them that socialism would also ultimately fail because when the reward is great, the effort to succeed is great, but when government takes all the reward away, no one will try or want to succeed.

These are possibly the five best sentences you’ll ever read and all applicable to this experiment:

You cannot legislate the poor into prosperity by legislating the wealthy out of prosperity.

What one person receives without working for, another person must work for without receiving.

The government cannot give to anybody anything that the government does not first take from somebody else.

You cannot multiply wealth by dividing it!

When half of the people get the idea that they do not have to work because the other half is going to take care of them, and when the other half gets the idea that it does no good to work because somebody else is going to get what they work for, that is the beginning of the end of any nation.

I hope you have enjoyed the latest edition of Noel News.

I hope you have enjoyed the latest edition of Noel News.

Thanks for all your kind comments. Please continue to send feedback through; it’s always appreciated and helps us to improve the newsletter.

And don’t forget you’ll get much more regular communications from me if you follow me on twitter – @NoelWhittaker.

Noel Whittaker