Noel News

“You cannot solve a problem

until you acknowledge that you have one

and accept responsibility for solving it.”

ZIG ZIGLAR

Welcome to our February Newsletter

It’s a big one this month, because a lot is happening.

Let’s start with yesterday’s interest rate decision. I am one of 32 “experts” who are surveyed each month on where we think interest rates are heading. This time the panel was split — 60 per cent tipped a rise, 40 per cent no change. I was in the no-change camp.

My reasoning was simple. February is when families feel the squeeze the most. The Christmas credit card bills arrive, school fees and uniforms have to be paid, and household budgets are already stretched. To my mind, this is the worst possible time to add another burden by lifting home loan interest rates.

Image by Freepik

The deeper problem is that interest rates are a very blunt tool. They only hit people with mortgages — mostly younger Australians who are working, raising families and paying the bulk of the tax income. Cutting their spending will not do one iota to rein in the inflation that is now embedded across the economy.

In the old days, policymakers believed you slammed the economy with rate rises or a credit squeeze. Businesses failed, people lost homes, demand collapsed and inflation fell. Those days are long gone.

Raising interest rates just six months after the RBA cut them is an admission that we have a serious long-term budget problem. The Reserve Bank says weak productivity sits at the heart of it.Government support — wage rises, tax cuts, energy rebates, infrastructure spending and a growing list of welfare measures — has kept consumers and businesses spending. That may have softened the pain, but it has also kept inflation alive. The RBA now concedes inflation will not return to the 2–3 per cent target band until mid-2027, still around 17 months away.

Most people are now forecasting at least two more interest rates in the next 12 months. All we can do is wait and see.

PODCAST

Making Money

Made Simple

with Noel Whittaker

Renowned broadcaster John Deeks and I discuss all the big topics covered in this newsletter in detail each month.

Tasmanian Trip

Time flies. In less than two weeks, we’ll be arriving in Launceston to start our tour of Tasmania. There’s been a big demand, and some of the events are sold out.

There will be five events in total — four organised by bookshops and one at Wrest Point Casino, organised by Shadforths, the most respected financial planning firm in Tasmania.

The biggest event will be at Wrest Point Casino in Hobart. As it’s an early evening event, they’ll be serving wine and canapés, and everyone will get a free book. Don’t miss your chance – event and registration details below.

Just keep in mind that bookstore events usually don’t have large spaces for audiences, and the bookstores are already promoting them through their own mailing lists. Some venues are limited to around 40 people, so please get in early if you’d like to come.

The bookstore events will be more like fireside chats, which allows maximum audience interaction. I’ll be talking about the state of the markets, where to invest, and all the usual topics covered in my books. Geraldine and I can’t wait to see you.

If you have any problems registering email me straight away at noel@noelwhittaker.com.au

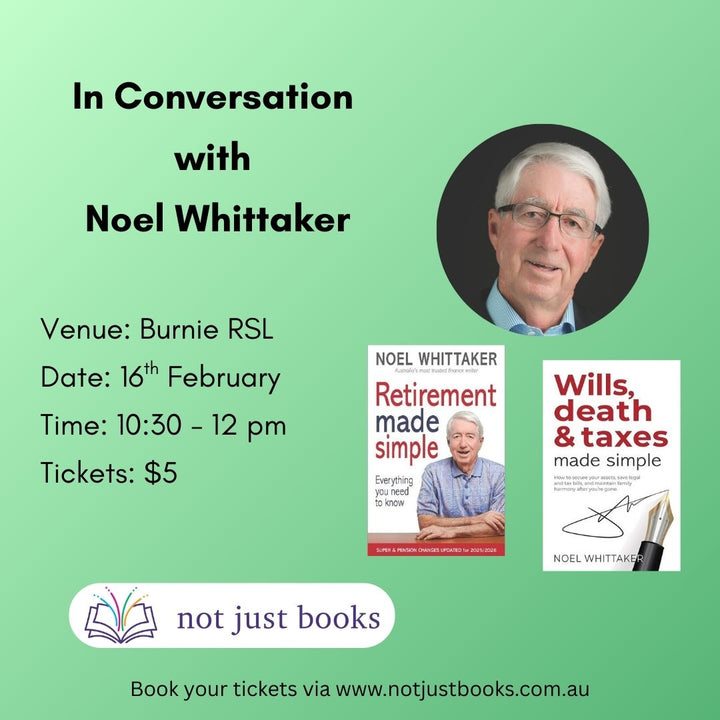

Monday 16 February – Burnie

Bring your questions. Numbers are strictly limited so book early.

Tickets available via the link below or in store.

WHEN

Monday 16th February

10:30am – 12pm

WHERE:

Burnie RSL

36 Alexander St

Rear entrance off Little Alexander St opposite the museum.

TICKETS:

$5

Tuesday 17 February – Devonport

WHEN

Tuesday 17th February

5:30pm – 7pm

WHERE:

Devonport Library – Level 1

Paranaple centre

137 Rooke Street, Devonport

Wednesday 18 February – Launceston

Wills, Deaths and Taxes book launch.

WHEN

Wednesday 18th February

10:30am – 12:00pm

WHERE:

Launceston Library

71 Civic Square, Launceston

Thursday 19 February – Hobart

I’m partnering with the team at Shadforth to host an event at the Wrest Point Casino on Thursday, 19 February 2026.

Wine and canapés will be served, and everyone will get a free book.

Shadforth have been looking after the wealth and retirement needs of Australians for over 100 years.

Come and hear from me, meet the Shadforth team, and learning how expert financial advice could you help you grow your wealth and plan the retirement you deserve.

Hurry – places are limited.

WHEN

Thursday, 19 February

5.30pm – 8.30pm

WHERE:

Wrest Point Casino

410 Sandy Bay Road, Sandy Bay

Wellington Room – Ground floor

RSVP:

WHEN

Friday 20th February

10am – 11am

WHERE:

Rosny Library

46 Bligh Street, Rosny Park

RSVP:

Potential changes to capital gains tax

Fasten your seat belts. Capital gains tax (CGT) is back in the firing line, and the forces pushing for change are better organised than ever.

In the lead-up to the 2019 election, Labor proposed halving the 50% CGT discount for assets held longer than 12 months to 25%. The Greens wanted the discount to be abolished entirely on investment properties beyond the first one. Both promised any changes would be grandfathered, meaning existing assets would be spared.

Last November, Labor and the Greens showed how effectively they could work together by passing the Environment Reform Bill. Then, on 4 November 2025, with barely a ripple of publicity, the Senate established a committee to examine the CGT discount. Its brief includes inequality (particularly housing), how the discount influences investment choices, and who really benefits. It was initiated by the Greens, who later said they would have no objection to reducing the discount for residential investment property. Treasurer Jim Chalmers has also openly flagged concerns about intergenerational inequality.

The ducks are lining up. Labor and the Greens have the CGT discount firmly in their sights, and this time there is no obvious reason changes could not make it through parliament.

The way it used to be

Let’s go back forty years to 1985. Back then, the top income tax rate was 60% on income above $35,000 a year and the company tax rate was a flat 46%. Paul Keating was the Federal Treasurer and hell-bent on tax reform. He initiated the National Tax Summit in July 1985, which led to a comprehensive tax package aimed at broadening the tax base, improving equity and reducing marginal tax rates to boost incentives for work and investment. Those rate cuts did not arrive overnight, but over the following years the top marginal rate fell sharply as the tax base was widened.

CGT was a centrepiece. The main selling point was that it was unfair to tax purely inflationary gains, so gains were indexed to inflation. It was also recognised that taxing a large gain in a single year at an individual’s top marginal rate was inequitable, so averaging was introduced. Under the system, individuals could divide the capital gain by five, add that amount to their taxable income in the year of disposal, calculate the extra tax payable, and then multiply that figure by five. The effect was to prevent capital gains from being automatically taxed at the highest marginal rate.

And it wasn’t just CGT on the radar. These changes were paired with major reforms to superannuation, including the introduction of a 15% tax on fund earnings, new reasonable benefit limits, tighter lump-sum concessions and proper integration of super into the income tax system. Super was deliberately repositioned as deferred wages rather than a tax shelter.

The next step came with the Ralph Review – a major overhaul commissioned by the Howard Government and delivered between 1999 and 2001. Chairman John Ralph’s brief was to make Australia’s tax system more competitive, more robust and less distortionary in a globalising economy. Its most important outcomes were a cut in the company tax rate from 36% to 30% and the replacement of the complex CGT indexation with a flat discount: 50% and 33.3% for super funds.

Today

This is broadly where the taxation of capital gains has sat ever since. The original concerns about taxing inflationary gains and the fair treatment of lumpy gains have largely faded from the debate, and the focus today is squarely on whether the 50% discount represents an excessive concession to higher-income earners.

Since then, the discount has been a constant topic of debate. Labor argues that it disproportionately benefits those wealthy enough to hold appreciating assets, encourages speculative investment in housing and has pushed home prices through the roof. The Coalition counters that discouraging investment in residential property would reduce supply and drive up rents.

A grandfathered change would also distort tax planning. Pre-change assets would become more valuable simply because of their tax treatment, while post-change investments would carry a permanent penalty. Matters become even more complicated if, as some propose, the changes apply only to residential property. If housing is taxed more heavily than shares or commercial property, capital will flow elsewhere.

Other options are on the table. The Grattan Institute wants to cut the CGT discount to 25% over five years, with no grandfathering, based on the date of sale rather than the purchase date.

Much of the push for change rests on the claim that investors are driving house prices. That’s wrong. Prices are high because demand has surged through strong immigration, supply is strangled by planning delays, and governments keep distorting the market with buyer subsidies. Pouring more money into a system with a limited supply only pushes prices higher, and then investors take the blame.

Image by Freepik

The big question

The big question is this: What sort of housing system do we want? Those on the left are pushing hard to make private investment in housing unattractive. If that continues, do they seriously believe the alternative is better? A dystopian future where the government becomes the dominant landlord, running rental housing through bureaucracy and regulation? Governments are not keen to take that on, and I shudder at the thought.

There’s more. CGT is calculated by adding the profit less discount to your taxable income in the year the contract is signed. Given our top marginal rate is 47%, including Medicare levy, the maximum effective tax rate is 23.5%. Cut the discount to 25% and the maximum effective tax rate jumps to 35.25%.

That number matters. As we saw with Treasurer Chalmers’ flirtation with taxing unrealised capital gains, 30% is the psychological and practical red line for tax planning: push tax above it and behaviour changes immediately. An investor deterred by a 35.25% CGT rate doesn’t stop investing; they simply invest differently. The same share exposure can be achieved through an insurance bond, where the maximum tax rate is 30% and capital gains disappear altogether after 10 years. Others will move investments into a family company, where tax is again capped at 30%.

|

|

|

Just tinkering around the edges

If the aim is to raise more revenue by increasing CGT, the biggest weakness in the strategy is that it tackles only one small part of the tax system. Everyone accepts that salary and wage earners already bear most of the tax burden, and because tax scales are not indexed, they pay more every year through bracket creep. At the same time, the fastest-growing group in the community is retirees, many of whom can legitimately shelter large sums in low-tax or tax-free superannuation. Any serious discussion about tax fairness has to acknowledge that reality.

From time to time, someone suggests retirees should simply “pay their fair share” by taxing all superannuation at a flat 15%. It sounds clever, but it wouldn’t work. A couple with $800,000 in super could withdraw the lot, invest in exactly the same assets in their own names, and still pay no tax. A typical $800,000 portfolio might produce about $37,000 a year in income and $27,000 in capital growth, on which no immediate tax is payable. In joint names, that’s tax-free. |

|

|

|

|

So, lifting CGT isn’t a solution. It distorts behaviour, shifts money around, and doesn’t raise tax revenue significantly. If we are serious about fixing long-term budget deficits, there is only one practical answer left: a broad-based, universal GST.

What now?

So, what will be the outcome? Forecasts are always a gamble, but let’s look at the facts. Labor and the Greens have long argued for the 50% discount to be reduced to 25%. With the numbers now in parliament, it would be reasonable to assume such a change could be legislated. The formal review of the CGT discount is due to report by 17 March, barely two months before the expected May federal budget. While there will be plenty of submissions, they will cover familiar ground, and it is unlikely the government will hear anything fundamentally new. That allows for a relatively swift decision. It is also clear that governments prefer to get unpopular decisions out of the way early in their term, giving voters time to move on before the next election.

It is therefore reasonable to assume the May budget will include an increase in CGT payable on assets acquired after Budget night, by reducing the discount for individuals from 50% to 25%. The discount for superannuation funds may also be lowered or even abolished. That would fundamentally change after-tax returns, particularly for leveraged property investors and those relying on asset sales in retirement years. It would also favour shares over property, because CGT on shares can be managed incrementally, while property forces you to crystallise the entire gain in one hit. |

|

|

|

The obvious question is: What should we do now? You must take advice and make up your own mind. But I see no rush to do anything before any announcements are made. Both the Greens and Labor have promised any changes would be grandfathered, meaning they should not apply to assets you already own. If you are thinking of acquiring a property in the next six months, it may be wise to do it sooner rather than later, but only if it represents good value. |

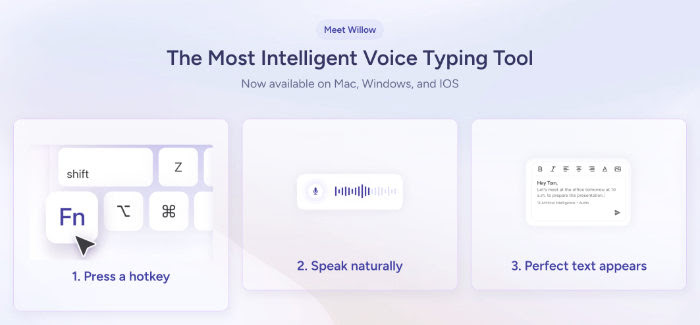

Willow Voice:

The app that changed my life

In my July newsletter, I wrote:

Two months ago my son James emailed me about a new app called Willow Voice, which was receiving glowing reviews in the US. I gave it a try, and it changed my life. These days, every time I write something in the paper, I receive over a hundred responses asking for more detail. With Willow, I simply tap a key and speak my reply. It types everything for me with no training, no special microphone and astonishing accuracy. It runs quietly in the background on my computer, and it’s made email a joy instead of a chore. Since I started using Willow, my entire workflow has changed. I no longer struggle to compose replies or waste time checking for typos, only to be asked later if I really meant what I wrote. I just talk, and the job gets done.

Now, seven months later, it tells me I’ve already dictated 168,000 words, saved 68 hours and achieved an effective typing speed of 118 words per minute. Seven months ago, Willow would only work on Apple computers, but now they’ve had a total upgrade and it works on Windows as well. This is a major breakthrough.

I’m now in regular contact with the Willow team in the US, and they’ve kindly offered my readers a free one-month trial. If it suits you, wonderful. If not, that’s fine too.

Quite simply, Willow has changed the way I work and I think it could change yours too.

Here’s your referral link:

https://willowvoice.com/?ref=

I’m very keen to hear of your experiences if you take up the offer.

Changes to the superannuation numbers

There are widespread rumours that the superannuation numbers will change on 1 July due to indexation. None of this is legislated yet, but based on the formulas used in the past, the figures being discussed are likely to be very close to the mark.

Image by Freepik

The big one is the transfer balance cap – the maximum you can move into tax-free pension phase – which is expected to rise from $2 million to $2.1 million from 1 July 2026. This increase would also lift the total super balance limit above which you can no longer make non-concessional contributions, currently set at $2 million.

The non-concessional contributions cap is also tipped to increase, allowing up to $130,000 a year in after-tax contributions, compared with $120,000 now. That would lift the three-year bring-forward limit to $390,000. The concessional contributions cap is more uncertain. It is widely expected to remain at $30,000 for 2025-26, but indexation could push it higher in 2026-27. We will not know for sure until the ATO formally confirms the numbers, but these are the figures most advisers are currently working with.

Ebooks – guidance in your pocket.

If you want to start reading the new Ebook editions of Super Made Simple 7th Ed and Retirement Made Simple 6th ed on your computer, Kindle or phone, you can find them in the Noel Whittaker Ebooks Store.

If you have previously purchased the Super Made Simple 6th Edition Ebook or Retirement Made Simple 5th Edition Ebook, you can upgrade to the latest editions for just $3.95. Your discount will be automatically applied at checkout, or use the discount code “RMSPrevious” for the Retirement Made Simple upgrade or “SMSPrevious” for the Super Made Simple upgrade. (Note it will only work if you are a purchaser of the previous edition).

What’s changed in the 7th Edition?

Contribution limits, tax rules, and Centrelink thresholds don’t stand still. This edition brings everything up to date for 2026.

- Latest contribution caps

- Current tax rules

- Updated Centrelink age & tests

- New thresholds and examples

- Investment performance data

- Clearer explanations and examples

- The 7th edition is updated with new SuperRatings performance data showing how investment choices can mean hundreds of thousands more in retirement.

- Complex Topics Made Simpler

-

- Retirement income streams

- Estate planning & death benefits

- Relationship breakdowns

- Transition-to-retirement strategies

RETIREMENT MADE SIMPLE

What’s changed in the 6th Edition?

This edition brings Retirement Made Simple fully up to date for 2026

- Updated Superannuation rules & caps

- Current Age Pension thresholds and tests

- Latest tax treatment in retirement

- Revised thresholds, figures and examples

- Updated discussion of legislative risk

- Clearer explanation throughout

- Greater coverage of emerging retirement income products and the growing importance of flexibility as rules continue to evolve

- Retirement income streams

- Superannuation & pensions

- Tax in retirement

- Estate planning & death benefits

And finally

AI does Dylan:

The Feeds They Are A-Scrollin’

Come gather ’round folks

Wherever you swipe,

And admit that your phone

Runs your day and your night.

There’s a headline for fear

And a take for each side,

And the truth’s in the comments,

Somewhere buried inside —

So loosen your certainties,

Hold ‘em with grace,

’Cause the feeds they are a-scrollin’,

And reality’s buffering in place.

Politicians keep talkin’,

AI’s learnin’ to sing,

Your fridge knows your habits,

Your watch knows everything.

Outrage is trending,

Nuance is not,

And yesterday’s scandal

Is already forgot.

If your map feels outdated

And your compass feels bent,

Don’t curse the confusion —

That’s just history being reinvented.

So prophets and podcasters,

Baristas and bots,

Stop prophesyin’ doom

From ergonomic spots.

If your truth needs a logo

And a limited run,

It’s already merch

Before it’s begun.

You can shout at the future,

Or argue with clouds,

But the times aren’t just changin’ —

They’re knockin’ on doors that don’t lead anywhere.

A big thank you to all you good people who read my newsletter.

If you were forwarded this newsletter by a friend and you would like to subscribe, you can do so here:

You can also find the subscription box in the footer of all website pages.

For more Noel News:

Download recent Noel News as a PDF

I hope you have enjoyed the latest edition of Noel News.

Thanks for all your kind comments. Please continue to send feedback through; it’s always appreciated and helps us to improve the newsletter.

And don’t forget you’ll get more regular communications from me if you follow me on X – @NoelWhittaker.

Noel Whittaker