Noel News

“Blessed are those who give without remembering

and take without forgetting.”

ELIZABETH BIBESCO

Welcome to our May Newsletter

The Reserve Bank has lifted rates again – the third increase this year. Predictably, the blame has been sheeted home to the war in Iran. But that doesn’t stack up.

Inflation was already running hot at 3.7 per cent to February, well before the conflict. By March it had jumped to 4.6 per cent as higher fuel costs rippled through the economy, pushing up not just petrol but a wide range of everyday expenses. Other countries also saw a lift in March, but ours remains higher than most.

The truth is that today’s inflation problem was largely home-grown and long in the making. Both the Reserve Bank and governments at every level played a part in the post-Covid blowout, yet both now prefer to point the finger offshore – first to Ukraine and now to Iran.

The reality is simpler. The Reserve Bank was late to recognise the inflation coming out of pandemic stimulus, and when it finally acted, it moved later and more cautiously than its global peers.

Then came an even more puzzling decision. In 2025, with inflation still above target, the economy running close to full capacity, unemployment low and wages under upward pressure, the Bank cut rates three times. That added fuel to the fire at precisely the wrong moment.

Interest rate policy matters more here than almost anywhere else. Australia has an unusually high proportion of variable-rate mortgages, which means households feel rate changes almost immediately. Add to that one of the most highly indebted household sectors in the world, and the impact is magnified.

As today’s Australian Financial Review cartoon shows, the government has its foot on the accelerator while the Reserve Bank has its foot on the brakes. Think about the $2 billion pumped into the economy to save people a few cents off their fuel bill, and the $20 million spent on advertising to teach us how to drive in a fuel-efficient manner. I dread what’s coming in next week’s budget.

Next Week’s Budget

Next Tuesday night Treasurer Jim Chalmers will deliver the 2026 Budget. There has been intense media speculation about what it might contain, but it pays to remember how governments operate. With a three-year term, any tough or unpopular measures are far more likely to appear in the first budget, giving voters plenty of time to forget before the next election rolls around.

Notice how the narrative has shifted. Until recently, the focus was on whether there would be changes to capital gains tax and negative gearing. Now the conversation has moved on to what the government will do with all the extra revenue it expects to raise from those changes.

To make things even more interesting, there is now talk of a special tax on family trusts. All I can say is: Watch this space.

Our next event

On Thursday, 21 May 2026, I will be partnering with RSL LifeCare to host an event at View Sydney, North Sydney. This will be an interactive presentation, with Rachel and I covering all the advantages and disadvantages of downsizing, as well as the key tricks and traps in aged care.

Since 1911, RSL LifeCare has been committed to serving the community by providing professional, compassionate support for veterans, and today supports senior members of the public, both veterans and non-veterans.

Booking is essential. I suggest you register quickly, – our events in Sydney normally sell out quickly.

WHEN

Thursday 21 May 2026 | 10am for 10.30am start to 1pm

WHERE

View Sydney Hotel, 17 Blue Street, North Sydney, NSW 2060

RSVP

PODCAST

Making Money

Made Simple

with Noel Whittaker

Renowned broadcaster John Deeks and I discuss all the big topics covered in this newsletter in detail each month.

The lucky country???

Australia is on a dangerous downward path. It’s been getting worse for years, but the tipping point for me was when our PM had to go to Singapore to beg for fuel.

Singapore imports everything – fuel, food, metals, building materials, even water – yet it has built a world-class refining and supply hub that services much of our region. Meanwhile, we ship our resources offshore and then buy them back in refined form.

The numbers beggar belief. Singapore, with a population of just 6.1 million and a land area of 719 square kilometres and with no natural resources, is outperforming a nation of 27.7 million people spread across 7.7 million square kilometres.

Interest rates in Singapore are about 1.0% versus our 4.1%; inflation, 1.2% against 3.7%, and government spending is just 16.8% of GDP compared with our 26.5%. Its top personal tax rate is 24% versus our 47%; company tax, 17% versus 30%, and unemployment, 2% against 4.3%. It runs a current account surplus of 16.7% of GDP, while we run a 2.9% deficit. It even holds more gold – 194 tonnes to our 80 – despite never mining an ounce. Its citizens live longer and emit less carbon per head.

Image source: MOH

The contrast is brutal. Singapore a nation with no natural resources has built a powerhouse economy in just over six decades. While Australia was born as a modern nation a hundred and fifty years ago and is now bogged down in bureaucracy and red tape, relying on exports to keep us going.

Our debt is now over a trillion dollars, yet the government’s approach to spending is reckless. When the fuel crisis got serious, the priority should have been to protect the budget and encourage people to use less fuel. Their reaction was to spend $2 billion, which will be added to our national debt, to save a few cents a litre. The next “solution” was to waste another $20 million to educate people to drive using less fuel.

Don’t get me started on NDIS. It started with good intentions, but has never been means-tested, and there are no apparent checks and balances on charges by providers. The cost has doubled since 2021, and is forecast to hit $55 billion next financial year, which is even more than our defence budget. Everybody has an NDIS story. Jack’s is typical. He told me his son is obese and needs a special chair. The price at Harvey Norman was $2,000, but after spending six months making an application to NDIS for the same chair, he discovered the cost was $6,000, which would be taken out of his NDIS package.

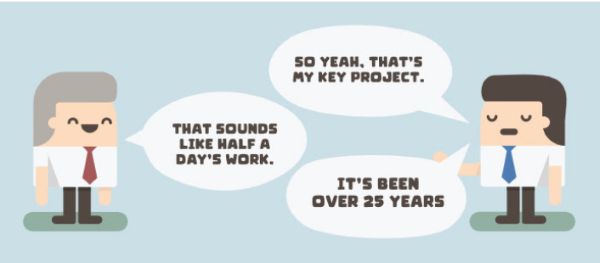

Then, of course, there is the inability for one state to agree with another. I was having lunch recently with John Chesterman, the Queensland Public Advocate, whose job is to improve laws, policies and services for vulnerable adults. He told me one of his key projects is to standardise financial enduring powers of attorney across all states and territories. I said that sounded like half a day’s work. He replied it has been going for more than 25 years, and they still cannot get an agreement.

Aged care is a complete dog’s breakfast. Governments have known for decades that an ageing population would place enormous strain on the system, yet they have failed to put in place policies to ensure enough beds and workers to deliver proper care. After years of scrutiny and the Royal Commission into Aged Care Quality and Safety, the 2025 reforms were hailed as “once in a generation”, promising a person-centred system built on dignity, respect and safety.

The reality is very different. Changes to fees and funding have left thousands of vulnerable seniors stranded in hospital beds while being labelled “bed blockers”. More than 100,000 are still at home waiting for care. The average wait for an aged care assessment is four weeks, based on a new algorithm many experts say underfunds or downgrades support. After that, the average wait for a package to begin is a further 245 days, and many wait far longer.

Image by rawpixel on Magnific

When care finally arrives, costs can be staggering. Changes to provider charges and new co-contributions – where self-funded retirees may pay up to 80% – have pushed prices to extremes: cleaning at $170 an hour, help with showering at $180, gardening close to $300, with higher rates after hours.

This problem will worsen before it improves. About 1.5 million Australians currently receive aged care; by 2050, that number is expected to reach 3.5 million.

It’s not that we lack resources. It’s that we’ve lost the ability to turn them into outcomes

In 1964, journalist Donald Horne published The Lucky Country, and the title became Australia’s enduring nickname. But most Australians missed his point. It was never a compliment. Horne wrote: “Australia is a lucky country run mainly by second-rate people who share its luck. It lives on other people’s ideas.” His message was clear: our prosperity owed more to luck and natural resources than to innovation or leadership. It was a wake-up call to an unimaginative nation, an indictment of a country drifting into mediocrity. Sixty years on, it reads less like history and more like a warning we chose to ignore. If there were a sequel today, the title might well be: Don’t Cry for Me, Argentina.

Scammers

Scammers have been with us for decades, and their activities have been well publicised. Most people now know the dangers of unsolicited phone calls and are savvy enough to ignore texts pretending to be from their children on an unknown number saying, “my phone has been stolen, and I need some money to help me out.” Despite all this, scammers still reaped more than $2 billion from Australians last year; their methods are becoming ever more creative and sophisticated.

I’ve been happily playing online Scrabble (Words with Friends) for many years. It’s a one-on-one game, and players usually have a photo or some random image. It’s largely anonymous, and there is rarely any contact with your opponent apart from the occasional “Merry Christmas” or “good game”. It has always felt like a safe and rather old-fashioned pastime.

But the landscape is changing.

Over the past year I’ve noticed more and more invitations from very attractive young women, often with a strategically chosen photo featuring an enticing glimpse of cleavage. That in itself is unusual enough in a word game, but curiosity gets the better of you. The game starts normally, then comes a casual question such as, “Where are you from?” You reply “Australia,” and they say they’re somewhere in America. Soon they ask if you’re married. When I reply that I am, with grandchildren, the answer is usually along the lines of “age is just a number”, followed fairly quickly by a suggestion that we move the conversation to Telegram so we can speak more freely.

That’s usually where I stop.

However, one day, purely in the interests of research, I decided to see what would happen if I kept going. I declined to move to Telegram but continued chatting within the game. What followed was quite extraordinary and went on for the better part of two months.

I met “Cassie”, who supposedly owned a hairdressing salon in South Carolina, and “Linda”, who claimed to be a three-star general with peacekeeping troops in Syria. Both were divorced, each had one child, and both quickly developed a keen interest in my life. Their stories were detailed, consistent and surprisingly believable. The conversations were friendly, sometimes flattering and always engaging.

But there was one constant. When I suggested something as simple as a FaceTime or Zoom call, the conversation ended abruptly. No excuses, no explanations – just silence.

Image by redgreystock on Magnific

So what was going on? I asked ChatGPT, which explained that this is a classic romance scam, often called a “pig butchering” scam – because you, the intended victim, are the pig being fattened up. The scammers invest time, sometimes weeks or months, building trust and emotional attachment before eventually asking for money. The photos are stolen from real people’s social media accounts, and many of these operations are run from compounds in Southeast Asia, often using trafficked workers under appalling conditions. My “friends” Cassie and Linda never existed.

The reason they try to move you to Telegram is that it allows anonymous accounts, has very little moderation, and takes the conversation away from the original platform where suspicious behaviour might be detected. It also makes it far harder for law enforcement agencies to track what is going on. Once you leave the original platform, you are effectively on your own.

Then came a completely different approach.

I received an email from a reader saying they had a throat infection and could not speak, and asking if we could communicate by email instead. It did not seem unreasonable – after all, people do get sick – so I replied. The response was a request to help a sick child get food, suggesting that a donation of $100 in cryptocurrency would make a big difference.

To me, it made no sense. It was such an obvious con that I could not see how any reasonable person would fall for it. But once again, ChatGPT explained the real purpose. They are not primarily chasing the $100. They are testing for engagement. They are building lists of people who will open, read and respond to emails of that kind. Once you engage, even out of politeness, your name goes onto a list as a potential target.

Sure enough, for the next three months I received a steady stream of emails from different people, all claiming to have throat infections.

Image by Brett Jordan on Unsplash

|

Identification challenges

Identification and verification are becoming major issues as scams become more prevalent, and they can create unexpected roadblocks. Those roadblocks can appear in surprising places, especially for Australians who were born overseas, or whose families were born overseas.

Image by labunsky on Unsplash

A reader recently wrote to me about his mother, who is 93 and living independently in Australia, but was born in Poland. They needed to draw money from her account to pay for aged care, but the name on her bank account is different from the name on her legal documents. The savings account has been in her name for years. But when the bank carried out the identity check that is now required, her documents did not match. She has no current photo ID: no passport, and no driver’s licence. All she has is a Medicare card and a pension card, neither of which includes a photograph. After a somewhat robust discussion with the bank, it finally accepted a combination of her Medicare card, Centrelink card and electricity bill.

These problems crop up in many areas. In everyday life, many people with names that are unfamiliar to English speakers, or simply long by English standards, keep their full legal surname but use a shortened version for convenience on bank accounts, email addresses and informal records. For example, a surname such as Chandrasekaran might simply be shortened to Chandra. That can cause problems later, when institutions require an exact match with legal documents.

That may sound like a minor administrative issue, but it becomes serious when money, health decisions or estates are involved. In those situations, exact identification is not just helpful; it is critical. Any inconsistency can cause delays, disputes and significant expense.

My legal friends tell me that they regularly see applications for probate held up because the deceased’s name on the will does not match their name on the death certificate. We once knew someone who called herself Marie, but whose other names on her personal papers ranged across Marie Anne, Maree Anne and Marie Ann. And the wildcard here is potential for hyphens to make it even more complicated.

Image by Melinda Gimpel on Unsplash

While we’re on the subject of estate planning, remember to keep your will updated. Many who get as far as making a will then fail to keep it current. As time passes, many events influence the way a will-maker would like to have their precious assets distributed. These include normal lifetime events such as death, divorce, remarriage and children being born, which is why it’s important to review your will every few years, or whenever a significant event happens.

And there is another major issue that is often forgotten: access. Just recently, I heard about an old bloke who had made his Enduring Power of Attorney (EPA), Advance Health Directive (AHD) and will. He then very carefully locked them in a safe deposit box at his bank. Sadly, this meant they were inaccessible to anyone but him without getting some kind of court order, which involved time and money.

The lesson to take from this is to make sure your family know where these documents are and how to get them. This applies particularly to the document that sets out your wishes if you become seriously ill or incapacitated – called an Advance Health Directive, Advance Care Directive or Advance Personal Plan depending on where you live in Australia. To be of use, this document must be readily accessible when you suffer an accident or acute illness.

A friend was telling me about her 94-year-old mother, a lonely widow in poor health, who was looking forward to passing on. One day she had a bad fall at home, but because her AHD could not be located (it was at the doctor’s office and it was the weekend), the paramedics were obliged to resuscitate her, which was against her wishes. Throughout Australia, medical staff must try to preserve life unless a valid document gives a relevant instruction to the contrary, such as “Do not resuscitate”.

Image by ageing_better on Unsplash

Remember too, that a major part of your estate planning should include an EPA. This gives specified people – normally family members – the right to make financial decisions on your behalf if you are unavailable, in poor health or, as we see increasingly, losing decision-making capacity. Unfortunately, human nature being what it is, these are often signed and filed away with the other estate documents until an unexpected event happens and the document is required urgently. But it’s always a good idea to test the document out long before you need it.

My son, who is an American resident, gave me power of attorney for his account at Bankwest, and it took them a week to approve it for use at their bank. Recently, I heard the case of a widow who had given her son and daughter an EPA. They were shocked to discover the document was invalid when they needed to withdraw $500,000 from a bank account to pay a residential aged care bond. The problem was that they had signed the document before their mother and it’s not legally possible to accept the power before it’s given. Legal advice was that it could easily be fixed by having the attorneys re-sign the paperwork. However, the bank would not accept that view, and a rigorous legal debate ensued. In the end, they had to go to court.

It’s a reminder not to take estate planning for granted. Long before documents are needed, make sure they exist, can be found, will actually work when you need them, and that names are consistently spelt on all the relevant records.

You may find my Executors’ and Attorneys’ Cheat Sheet useful. This prompts for many kinds of information relevant to enabling your attorney/s and executor/s to carry out your wishes, including the issues covered in this column. It is available as a free download at

From the mail box

From the mail box

I read your first book when I was about 20 around 1990, and then More Money [now Making Money Made Simple] in 1995. I’m now 55. I left home and school at 16 in 1986 with less than $100 in my pocket and joined the Navy to get a trade, finishing Year 10 along the way. I jumped on the “magic train” around 1990 or 1991 at about Station 7, and 35 years later I reckon I’m somewhere around Station 42.

Chapter 3, “Why only 8% make it financially”, and the Fairy Godmother story made all the difference for me. My first major investment was a property in Perth, which I bought for $65,000 in 1991. I still own it and have had the same tenant since 1993.

Image by freepik

Your books, along with Money magazine in its heyday, gave me the insights I needed. These days I live in Victoria, in a modest three-bedroom home with my wife, and I’ve been debt-free for years. Thank you for deciding to write that book back in 1995, and thanks to your wife for pushing the go button.

A timely reminder…

and a few good books to go with it

This month’s newsletter has touched on budgets, rising costs, scams, and the growing complexity of everyday life. Most people don’t think much about these issues until they are right in front of them — a tax change, a phone call that doesn’t feel quite right, or a family situation that suddenly needs decisions made quickly.

The truth is, a lot of stress in later life comes down to not having clear information when it’s needed.

That’s where a good book can quietly do a lot of heavy lifting.

If you want a straightforward guide for yourself, Wills, death & taxes made simple is designed to cut through confusion around estate planning, pensions, tax and what actually happens when life gets complicated. It’s the sort of book many people keep and come back to when they need to make decisions.

And finally

|

|

A big thank you to all you good people who read my newsletter.

If you were forwarded this newsletter by a friend and you would like to subscribe, you can do so here:

You can also find the subscription box in the footer of all website pages.

For more Noel News:

Download recent Noel News as a PDF

I hope you have enjoyed the latest edition of Noel News.

Thanks for all your kind comments. Please continue to send feedback through; it’s always appreciated and helps us to improve the newsletter.

And don’t forget you’ll get more regular communications from me if you follow me on X – @NoelWhittaker.

Noel Whittaker