Noel News

Experience is a comb that nature gives us when we are bald.

CHINESE PROVERB

Welcome to our latest Newsletter

To start I share a personal experience with our travels, the unexpected, and our travel insurance coming to the rescue. In this issue, we’ll dive into the 2025 aged care reforms and explore how they’ll impact you financially. Plus, I’ll walk you through the latest pension numbers and why I highly recommend downloading the new pension charts and testing out the age pension and deeming calculators on my website. We’ve also got some tips on building wealth and another powerful testimony from a reader who’s successfully applied the principles in my books to achieve financial success. Enjoy the read!

The “joys” of travel

The “joys” of travel

In my last newsletter, I told you how Qantas had cancelled our flight home from Los Angeles and rescheduled us to a flight to depart on the following Tuesday at midnight.

At 6 pm on the day of departure Geraldine went for a walk and had a fall. It was not life-threatening but she passed out on the footpath. Luckily a passer-by used her phone to call me. We called 911 and two huge fire engines with a team of seven paramedics turned up.

Image by stefamerpik on Freepik

Apart from some abrasions on her arm and a possibly sprained right wrist, she appeared to be okay but of course had to go to the hospital to be checked. They did all the usual tests, including an X-ray and CT scan, and said she was good to go home but not to fly that night.

That meant an urgent call to the travel agent to cancel the midnight flight and get us on something else. They got us a non-stop business class flight to Brisbane leaving Tuesday night and arriving at 5 am on Thursday. The cost of changing fares was $12,000, which I am in the process of claiming on travel insurance.

Because of our age difference, we have two travel insurance policies. Geraldine has the automatic insurance that goes with our American Express card, provided we pay the tickets with it. But because I’m over 80 years old I have to buy my own separate travel insurance. Once again I used Medibank and the policy cost $1,092 for the return trip.

The hospital bill for Geraldine’s two-hour stay, X-rays and CT scan was A$5,155. So we’re claiming $11,155 for her – the changing fares and the medical costs. My own claim was just $6,000 for the cost of changing flights. I will keep you posted as to progress but so far it’s been slow and frustrating. It certainly highlights the value of booking your airfares with a credit card that has automatic travel insurance.

I tried to use my Latitude credit card to pay the hospital bill and received a text asking to press 1 to approve a charge for $5,155 and 2 to reject it. I pressed 1 but the card was still declined. Latitude encourages customers to use their app for communication but when I started a conversation I was astounded – I typed in “a payment of mine has been declined” and the automatic response was “I’m just a bot – I don’t understand the question.” I think AI has a long way to go in this field. This meant I had to ring them, which I could only do when their office was open. When I finally connected, I was told there was a 40-minute wait. Finally I spoke to a person who approved the payment and I now have a receipt to put with my travel insurance claim.

Aged care reforms 2025

by Rachel Lane

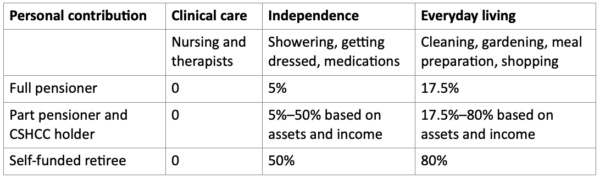

Next year marks the biggest aged care reforms in almost 30 years. The changes, described as “once in a generation”, will redefine aged care and who pays for it. The fundamental change is that the government will fund care for everyone (regardless of means) but those receiving care will need to pay more towards non-care services. So the critical question is, what is care? It is being defined as clinical care, i.e. those services provided by a nurse or therapist. That makes the list of non-care services extensive: from help with taking medications, showering and dressing, through to tasks like shopping, gardening and preparing meals.

Although many people think of aged care as being in nursing homes, most services are actually delivered at home; of the $5.6 billion reform package, around $4.3 billion will go to home care.

Image by DC Studio on Freepik

Home care

Support at Home will bring together the home care package and short-term restorative care programs. It will also introduce an Assistive Technology and Home Modifications Scheme up to $15,000, and an End of Life Pathway offering up to $25,000 of funding for palliative care.

Support at Home services will be classed as clinical care, independence or everyday living. The government will fund all clinical care, and you will pay on a sliding scale towards the other services, based on your assets and income. Maximum funding for a Support at Home package will be $78,000/year.

Case studies: Support at Home

Jill, a full pensioner with $10,000 of assets, will pay $2,467/year (government will pay $37,107).

Marco, a part pensioner with $65,000/year income and $200,000 in assets, will pay $11,464/year (government $28,110).

Robin, a self-funded retiree with $100,000/year income, and assets of $500,000, will pay $16,615/year (government $22,959).

Image by rawpixel on Freepik

Aged care homes

The first change to the cost of aged care homes will actually come into effect on 1 January 2025, with the market price cap on refundable accommodation deposits (RADs) increasing from $550,000 to $750,000. The cap is the maximum price a home can charge without government approval.

From 1 July 2025, aged care homes will also charge an exit fee of 2% of your RAD per year, for up to 5 years. So if your RAD is $750,000 and you stay for 5 years, $75,000 will be deducted when you leave. People who pay by daily accommodation payment will have their fee indexed by CPI twice a year, rather than paying a fixed rate based on their entry date.

The reforms don’t change who is eligible for support with aged care accommodation costs: people with assets above $206,039 will need to pay the market price. If most prices go up to $750,000 there will be a $500,000 gap between what some people need to pay and what they can afford.

When it comes to the ongoing cost of your aged care, the government will pay for clinical care. Everyone will pay the basic daily fee (BDF), set at 85% of the age pension. Beyond this you will pay a hotelling supplement to cover services such as cleaning and laundry, a non-clinical care contribution based on your assets and income, and a higher everyday living fee if you choose to get “extras”.

There is no change to the means testing of the family home: it is included up to a capped value of $206,039 unless a protected person lives there, in which case it is exempt.

Summary: what an aged care home will cost you

Accommodation: the new market price cap is $750,000. Each year, 2% will be deducted from your RAD, up to a 10% cap.

Basic daily fee: $64/day or $23,200/year is paid by everyone, regardless of means.

Hotelling supplement: users pay 7.8% of assets above $238,000, or 50c per dollar of income above $95,400/year, up to $13/day or $4,600/year.

Clinical care is paid for by government; no individual contribution is required.

Non-clinical care contribution: users pay 7.8% of assets above $502,981, or 50c per dollar of income above $131,279/year, up to $101/day or $36,923/year, and capped at 4 years and $130,000.

Higher everyday living fee: user pays for services such as hairdressing, or beer/wine with meals.

Case studies: Residential aged care

Hannah is a full pensioner who owns her home and has $150,000 of assets. She will pay $28,800/year (government will pay $111,300). As she currently pays $24,700/year, this is an increase of $4,100/year.

George is a part pensioner who owns his home, and has additional assets of $500,000. He will pay $47,700/year (government $92,400). He now pays $34,300/year, so he will pay $13,400 more each year.

Heather is a self-funded retiree who owns her home, and has $70,000/year income and $500,000 assets. She will pay $62,800/year (government $77,400), a $13,400 increase on her current contribution of $49,400/year.

“No worse off” principle

The no worse off principle is designed to protect people already receiving aged care, or eligible for a home care package but waiting for it to be delivered. It means that your costs will be the same or less after the reforms. If you move from home care to an aged care home after 1 July 2025, the changes to accommodation payments will apply, but you will have the choice of staying on the existing contribution arrangements or moving to the new ones. If you are already living in an aged care home, or move in before 1 July 2025, your contributions will not change while you live there.

The government estimate that 3 in 10 full pensioners and 3 in 4 part pensioners will pay more; it’s easy to see why. While the message has been that “wealthy Australians will pay more for aged care,” it seems most Australians will pay more – in some cases, much more.

The new pension numbers

The quarterly age pension adjustments came into play on 20 September, and thanks to inflation all pensioners got an income boost. The pension rates are somewhat confusing because there are four changes a year: in July and January each year they adjust the thresholds, and in September and March they adjust the amount of pension paid. These changes can sometimes produce anomalous outcomes, and savvy pensioners should keep an eye on the changes, to see if they can tweak their situation to achieve better financial outcomes.

Go to my website, www.noelwhittaker.com.au, to download the new pension charts and play with the age pension calculator and the deeming calculator, both of which have been updated with the new numbers.

The previous pension changes took effect from 1 July. Because they raised the thresholds but not the amount of the pension itself, only part-pensioners got an increase in their pension. This meant the neediest pensioners – those under the asset and income thresholds – got no pension increase at all, despite record inflation. In fact, they went backwards. But part-pensioners who were just over the bottom threshold ended up with a full pension because of the threshold increase.

Image by Freepik

When the rate of pension goes up, the upper limit threshold cut-off point automatically increases as well – the cut-off point for a homeowner couple has just risen to $1,045,500.

Note how the tests intersect: Centrelink tests you on both the income test and the assets test, and then applies the one that gives you the least pension. But the tests are out of kilter, which can lead to some unusual results. For example, if you’re asset-tested, deeming is not relevant – it’s only used for the income test.

The question I get asked the most is: How does Centrelink assess the pension I draw from my superannuation for the income test? They do not assess how much you draw. Your superannuation balance is given a deemed income and that is the one used for the income test. For example, if you were income-tested with $300,000 in super, your deemed income would be $180 a fortnight irrespective of what you were drawing out of your fund.

A couple with $960,000 of assessable assets can earn a yearly income of $95,000 because they’re not assessed under the income test. If those assets included $900,000 of financial assets, they would be assessed as having a deemed income of just $18,246 a year, but they would still have scope to earn an additional $76,754 a year.

Your own home is not assessable, but your furniture fittings and vehicles are assets tested. Many pensioners fall into the trap of valuing them at replacement value. This could cost them heavily because every $10,000 of excess assets reduces the pension by $780 a year. Make sure these assets are valued at garage sale value, not replacement value. This puts a value of $5,000 on most people’s furniture.

There are now pension-friendly products that may enable self-funded retirees to get a part-pension and all the concessions to go with it. For example, a couple with $1.1 million of assessable assets could invest $300,000 in an approved lifetime income product. The term “approved” means that only 60% of its value is assessed for the assets test – it’s as if they’ve disposed of the other 40%. Their assessable assets would drop by $120,000 to $980,000 and they would qualify for a pension of $97 a fortnight each, plus all the concessions. They would also receive a lifetime income from the new product, which could be worth $20,000 a year, indexed, depending on their situation.

If you think this sort of strategies may benefit you, talk to a good financial adviser for more details.

Building wealth

I recently had the honour of addressing doctors at a medical conference in Queenstown, NZ on building wealth. I’d like to share with you a part of what I told them.

The secret to a financially secure retirement is to accumulate a pool of capital. If you arrange your affairs properly and use the right investment vehicles, your capital will go on forever, increase continually, require minimal effort on your part, and be taxed at a much lower rate than income from personal exertion. But how do you build up sufficient investments to provide an income you can live well on?

The answer is by understanding the mathematics of compound interest. In 1748, Benjamin Franklin said, “Time is money” and this applies to both borrowing and investing. Suppose you had a loan of $800,000 on a 30-year term; your repayments would be $4,800 a month, and over those 30 years you would pay back a whopping $930,000 in interest. The long term means time is working against you. If you increased the payments to $6,800 a month, you would reduce the term to 15 years and the interest by $520,000. Interest on your home loan comes from after-tax dollars, so for a doctor in the top tax bracket, a saving of $520,000 after-tax dollars is equal to a boost in gross income of $982,000. The interest saved is equivalent to an extra $65,000 a year gross income over 15 years.

Looking at the other side of the coin, you can see the exponential effect of regular investment. To make time your friend when investing, you need as long a term as possible. You see, compounding takes time to work its magic, but the effects grow faster and faster as time passes.

Think about a 30-year-old professional who has $100,000 in superannuation. If they are in the top tax bracket, they will pay a 30% contribution tax, so yearly tax-deductible contributions of $30,000 will add only $21,000 to their super balance after the entry tax.

If they put their faith in compounding and set up a direct debit to ensure that $2,500 is transferred from their bank account every month into superannuation, I can assure you they won’t miss it. And it’s a tax deduction. After five years their super should be worth $270,000 – no big deal – but after 10 years they will have cracked the half-million-dollar mark, which is a nice nest egg for a 40-year-old. On their 50th birthday the balance should be $1.4 million, and the earnings in that year should now be over $100,000 – nearly five times their net contribution. The compounding process is now feeding itself. At age 60, they will have $3.4 million, and at 65, a huge $5.1 million.

I went on to explain the essential ingredient of wealth building, which I have always called “the guaranteed secret of wealth”: the easiest way to get ahead financially is to make investing the first expense out of your pay packet, and not something you try to do with what’s left over. This takes advantage of our propensity to get paid, pay our commitments, and spend the balance.

To give an example, back in 1980 everybody paid their home loans monthly. That is, until I stirred up the banks by telling people – on national TV – that they could save a fortune in interest if they made their payments weekly or fortnightly, instead of monthly.

Think about a couple paying $4,000 a month on their home loan. If they changed their payments to $2,000 a fortnight, they would pay an extra $4,000 a year without feeling it: there are 12 months in the year but 26 fortnights: each year, they make one extra payment. And because that money comes out before they even see it, the extra payment is painless.

Becoming wealthy is not rocket science – all you need to do is adjust your home loan repayments to the level suggested above, put a direct debit in place for your monthly superannuation contributions, and leave the rest to the magic of compound interest.

From the mailbox

“Hi Noel – I’m another of your “success stories”.

When I was growing up, my parents were always bickering about money because they weren’t very good at managing it, and I was determined not to fall into the same trap.

In 1993, as a young uni student, I bought your books Getting It Together and Making Money Made Simple and from then on diligently applied your principles and worked hard.

Thirty years later, I’m 56 and on track to step back from the paid workforce when I’m 60, by which time I’ll have a portfolio of over $6M in shares, super and property.

My heartfelt thanks for your positive influence on my life!”

This reinforces what I told the doctors but also shows the value of time and perseverance. It’s taken them 31 years to build a fortune – most people don’t start, or let life interrupt what they’re doing, and give it up.

Making Money Made Simple & Beginner’s Guide to Wealth

$49.95 inc. free shipping

By the way, the book Getting It Together has been rewritten and is now Beginner’s Guide to Wealth. It’s not a book about money – it’s a book that teaches the principles of a successful life.

And finally

Why is “dark” spelled with a k and not c? Because you can’t see in the dark.

Why is it unwise to share your secrets with a clock? Well, time will tell.

When I told my contractor I didn’t want carpeted steps, they gave me a blank stare.

Bono and The Edge walk into a Dublin bar and the bartender says, “Oh no, not U2 again.”

Prison is just one word to you, but for some people, it’s a whole sentence.

Scientists got together to study the effects of alcohol on a person’s walk, and the result was staggering.

I’m trying to organise a hide and seek tournament, but good players are really hard to find.

I got over my addiction to chocolate, marshmallows and nuts. I won’t lie, it was a rocky road.

What do you say to comfort a friend who’s struggling with grammar? There, their, they’re.

I went to the toy store and asked the assistant where the Schwarzenegger dolls were and he replied, “Aisle B, back.”

What did the surgeon say to the patient who insisted on closing up their own incision? Suture self.

I’ve started telling everyone about the benefits of eating dried grapes. It’s all about raisin awareness.

A big thank you to all you good people who read my newsletter.

If you were forwarded this newsletter by a friend and you would like to subscribe, you can do so here:

For more Noel News:

You can also find the subscription box in the footer of all website pages.

I hope you have enjoyed the latest edition of Noel News.

I hope you have enjoyed the latest edition of Noel News.

Thanks for all your kind comments. Please continue to send feedback through; it’s always appreciated and helps us to improve the newsletter.

And don’t forget you’ll get more regular communications from me if you follow me on X – @NoelWhittaker.

Noel Whittaker