NOEL NEWS

“What lies behind us and what lies before us are tiny matters compared to what lies within us.”

GARTH BROOKS

Welcome to our March newsletter!

As always, there’s plenty to discuss.

Today, I’m covering the Reserve Bank’s latest decision, which all but guarantees that interest rates are heading down. I’ll also offer my take on the share market, delve into the wild story of how our NBN got swiped, reflect on the craziness of crypto, and break down the latest superannuation figures.

On a personal note, I’m thrilled to be giving five talks this month – hope to see some of you there!

Lastly, changes to the age pension are expected to be announced soon. I’ll post the updated numbers on my website as soon as they’re out.

Enjoy the read!

The Podcast

Renowned broadcaster John Deeks and I discuss all the big topics covered in this newsletter in detail each month.

The share market

I must confess, it hasn’t been an exciting start for share investors, with prices falling across the board – both here and overseas.

Cartoon by Bob Rich for Hedgeye

But as unsettling as it may be, we need to accept that volatility is the price we pay for the liquidity of shares – they can be sold quickly, in whole or in part.

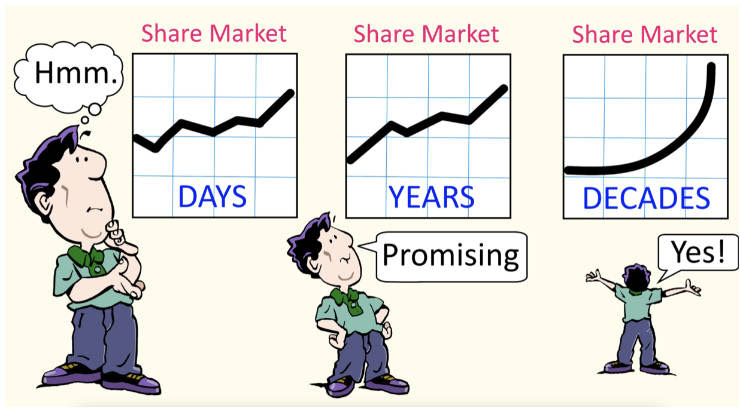

Keep in mind that over the past 120 years, the Australian All Ordinaries Index has delivered an average return of around 9% per year, including both income and growth. There are good years and bad years, but history tells us that in every decade, markets tend to produce six strong years and four weaker ones.

The secret is to hang in there.

Warren Buffett often uses a farm analogy to explain how investors should approach stock market volatility. “If you owned a farm and your neighbour came by every day offering to buy it at wildly different prices, you wouldn’t sell it cheap just because he was in a bad mood, nor would you think it’s worth a fortune just because he’s overly excited one day.”

The same principle applies to shares – focus on long-term value rather than short-term fluctuations.

Upcoming speeches

We’re coming to Sydney

Rachel Lane and I will share the dos, the don’ts, and the most important factors you should consider before downsizing.

Brought to you by RSL LifeCare – committed to creating a new benchmark of community for veterans and seniors in the Northern Beaches.

Register below for one of our four high tea events and hear from both speakers.

26 March Wednesday

From 10am, for a 10:30am start till 1pm

Long Reef Golf Club

Pacific Room

Anzac Avenue, Collaroy

27 March Thursday

From 10am, for a 10:30am start till 1pm

Norths Cammeray

Auditorium

12 Abbott Street, Cammeray

2 April Wednesday

From 10am, for a 10:30am start till 1pm

Killara Golf Club

The Dining Room

556 Pacific Highway, Killara

3 April Thursday

From 10am, for a 10:30am start till 1pm

Manly Golf Club

The Apperly Room

38-40 Balgowlah Rd, Balgowlah

See you in the Gold Coast

Centaur Financial Services invites you to an exclusive morning of financial insights and expert analysis at the beautiful Currumbin RSL.

Enjoy freshly brewed coffee or a selection of fine teas as you gain clarity and practical tools to help you confidently navigate today’s financial landscape.

Hugh will break down the key measures of the Federal Budget (if handed down on March 25th) and provide valuable investment and business updates to keep you informed in an evolving financial environment.

Noel will share essential insights on retirement planning, tax-effective investment strategies, and estate planning, helping you make informed financial decisions for the future.

Book Signing: As a gift from Centaur Financial Services, each attendee will receive a copy of one of my bestselling books.

This is a complimentary event, but spaces are limited!

Ducks and eagles

– how our NBN was stolen

It was a quiet Friday – tasks done, tea in hand. Life was good. Then, ping! an email arrived.

My heart skipped a beat when I read, “We are sorry to see you go,” from Aussie Broadband. Go? I hadn’t gone anywhere! Aussie had been a perfect provider for years, had never let me down. Yet, according to this email, I was leaving. I called them urgently.

Now let me tell you, when you deal with big companies, you quickly learn there are two kinds of people: ducks and eagles. The ducks waddle around making a lot of noise without actually doing anything. The eagles, on the other hand, soar high, spot the problem and swoop in to fix it.

Image by wirestock on Freepik

Sadly for me, I got a duck first up. The explanation I received left me both alarmed and incredulous: another provider (whose name they couldn’t disclose for “privacy reasons”) had applied to transfer the internet service at my address to another customer, whose name they also couldn’t give me for “privacy reasons”. That’s right: I wasn’t allowed to know who had told which provider to give them the internet service at my house.

Alarm bells went off. How could someone simply supply a false address to another provider and steal my NBN connection? This wasn’t just about losing the internet – though that would be serious enough – our home security system relies on that connection. I pressed for a resolution. “We need permission from the other provider to reclaim your line,” they quacked. When I called back for an update, I was met with another bureaucratic gem: “The other provider is refusing to cooperate.”

By next morning I’d had enough. I rang Aussie Broadband again, this time making it clear I’d involve the fraud squad if the issue wasn’t fixed immediately. And that’s when I struck gold – I got an eagle. Within an hour, my internet was restored.

Image by Freepik

But to get my own NBN service back, I had to provide proof of residence, which raised a troubling question: How could someone else hijack my address without similar verification?

Because of the gravity of the situation, I lodged a formal complaint with the

Telecommunications Ombudsman (TIO). This wasn’t an administrative error; it was identity theft. Two days later, Aussie Broadband confirmed the other provider involved was M2. But they still couldn’t tell me who had initiated the fraudulent transfer.

So, I rang the TIO – this time determined to get some answers. I got a duck.

“Well,” he said, “the issue here was your loss of NBN, and now you have it back and you are still with Aussie Broadband; that’s the end of the matter.”

That was not the end of the matter as far as I was concerned. I thought about it for a while longer, and then rang back. This time, I got an eagle. “No worries,” he said, “let’s lodge a formal complaint against M2.” The fight was on.

The next step was a phone call from Commander, who told me they were part of the M2 system and were trying to find out who had initiated the illegal transfer. Then, out of the blue, I got a phone call from the Philippines. A woman from Dodo – another part of the M2 group – explained the situation.

Her explanation was breathtaking in its simplicity: “We received an online application with your address,” she said, “and we processed it immediately.”

“Surely you check ID?” I asked.

“That’s NBN’s job,” she replied.

That made no sense, so I rang the NBN Media team. This time, I struck the jackpot and got a super eagle. He confirmed that NBN does not check the ID of people applying for services. They leave that to the retail service provider (RSP) that instigates the transaction. Then he told me something interesting.

A revised industry code is coming in a few months that will introduce a transfer validation process. This would require an AVC ID – a unique identifier that would work in the same way banks use account numbers. Once the system is in place, to move between retail service providers, customers on the NBN network would need to share their AVC ID with the new provider. In other words, the problem I had just untangled would soon have a solution.

That’s great news, but I feel sorry for anybody who goes through what I did in the meantime. And one thing is clear: irrespective of the institution you deal with, so much of the outcome depends on whether you get a duck or an eagle. Every company has both.

Interest rates

The Reserve Bank has spoken, and interest rates have finally been trimmed by 25 basis points. Some commentators were predicting this would kick off a parade of cuts, but Reserve Bank Governor Michele Bullock put that notion to bed fast. She made it crystal clear the decision wasn’t unanimous – there was serious debate about holding steady – and we shouldn’t expect a cascade of reductions anytime soon.

It was the right call, but it highlights the tightrope Australia is walking. Inflation isn’t just high; it’s embedded. For years, our only tool to control the economy has been monetary policy: raising rates to curb a boom, lowering them to fight recession. But much is now beyond the Reserve Bank’s control. Thanks to poor government policies, energy costs are soaring – everyone is feeling the pinch on food and fuel. And the country is in a massive construction boom, with labour and materials in short supply; both major parties want to ramp up home building, so there’s no relief coming for building costs.

Treasurer Jim Chalmers just couldn’t help himself. Fresh from basking in falling interest rates, he’s now calling on landlords to pass on the savings in rent. If he spent less time in Canberra and more time on the ground, he’d know interest isn’t the big killer; land tax is. In Queensland, it’s off the charts because the government has kept the thresholds frozen for 16 years. It’s a rort, plain and simple.

Of course, rate cuts are a double-edged sword. They help potential borrowers qualify for mortgages, but because this increases demand, they may also drive up the price of the very house a first homebuyer hopes to purchase.

There was media chatter about how this rate cut might help small businesses. Let’s be real: they’re at the banks’ mercy and currently paying much higher interest rates than homeowners. No small business owner is paying just 6% on a loan; it’s far higher. And a 0.25% cut won’t touch their real issues, which are soaring energy bills, rising wages and weak productivity.

There were many questions to my talkback radio show last Wednesday from self-funded retirees. The main theme What should I do now? I’ve just had a pay cut. I told them they could get an instant pay rise by shifting idle cash – eroded by inflation – into an index fund. That way, they’d earn 4.8% plus franking credits.

I pointed listeners to a recent newspaper article comparing asset allocations in major super funds with SMSFs. The reason SMSFs often underperform is that they hold a much bigger proportion of their assets in cash and tend to avoid international shares, which have been the best performers over the past decade.

In my view, cash is one of the riskiest investments. It offers no capital growth, no tax benefits on income and, worst of all, inflation erodes its value by at least 3% a year. Sure, retirees should keep three years’ worth of expenses in cash or reliable income. But this rate cut is a wake-up call: check your asset allocation and consider shifting more into shares.

Whenever I give a speech, I ask the audience to put their hands up if they understand the franking system; the response is always puzzled looks. That’s a sad reality because franking is one of the greatest assets for retirees. A nominal dividend of 4.8% turns into 6.9% when franking credits are included. And capital growth, averaging 4.5% over many years, is the cream on the cake.

The key takeaway? Inflation continues to eat away at cash, small businesses are doing it tough, and homebuyers could be looking at even higher prices. This rate cut should serve as a wake-up call, especially for retirees, who need to make their money work harder. That means taking advantage of franking credits, investing in quality shares and staying ahead of economic trends. Any benefits for homebuyers may be short-lived. Right now, all the headlines are about how the rate drop has driven property prices even higher.

Crypto fools on a hiding to nothing

More and more people are becoming fascinated by cryptocurrency. Today, I’m sharing an edited version of an article that appeared in The Australian on Thursday, 27 February. I think it’s brilliant.

“Crypto is the Seinfeld of investments. An investment in nothing. Sure, an investor in any one of the myriad coins will receive a digitized piece of paper with some numbers on it, but can you touch crypto? Can you smell it? Can you lick it?

The answer to that is no unless you’re a North Korean hacker. North Korea’s state-owned Lazarus Group has been diligently ripping off crypto investors, cracking open wallets and generally causing mayhem for the past decade.

In the latest episode last week, the lads from Lazarus ripped open a wallet filled with Ethereum held by the Dubai-based ByBit exchange and helped themselves to $236 billion worth of crypto goodies.

The volatility of crypto is breathtaking. Bitcoin pierced the $US100,000 mark largely on the election of Donald Trump last year. It was, crypto investors thought, the beginning of a golden age for investing in nothing. Yet when Donald Trump failed to mention crypto in his inauguration speech, the price of crypto plunged. Tariffs and trade war talk have not helped either. Bitcoin rallied briefly and hit a record high of $US106,000, but in trading on Tuesday, it was down to a more modest $US88,000.

On a much smaller scale, the Central American republic El Salvador went head-on into crypto, declaring Bitcoin the nation’s secondary currency in 2022. The greenback has been the primary currency since 2001. The crypto pitch to El Salvadorans was $US40 of free Bitcoin through the state-run payment system, which some helped themselves to, cashed in, and never darkened the doors of the payment system again.

The system completely failed to check users’ photos, relying solely on the state’s national identity card number and date of birth. Unsurprisingly, massive identity fraud occurred and the 40 sovs on offer were lifted under the nose of the large bulk of El Salvadorans.

Meanwhile, the world of meme coin has taken an even bigger hit, which is unsurprising as meme coins are little more than digitized penny stock pump-and-dump schemes.

Investors who bought the $Melania coin, issued two days before the Trump inauguration, are facing a wipe-out. Released at $131, the coin hit a high of $2163 on inauguration day. Investors can buy as many as they want now at $1.14. $Trumpcoin, issued on the same day, still sits above its launch price of $13.58 but its high-water mark of just under $120 lasted only a few days, with the price now sitting down at $20.

Visiting meme coin investor pages like pump.fun is like taking a fatal walk into a casino full of fools soon to be parted from their money—if they haven’t been shaken down already. The atmosphere is one of stoic gloom. They know they are being taken to the cleaners by forces beyond their ken but opt to stay in for fits and giggles.

Image by Bob Rich for Hedgeye

The problem with crypto and meme coins is that they are based on the principle of controlled scarcity and appeal to a get-rich-quick mentality. Investors might be squeaky clean, but they are still investing in something littered with mass-murder money, drug money, North Korean stolen money. The big problem North Korea’s Lazarus Group now faces is one of laundering their ill-gotten gains. The best guess is they will be trying to convert their stolen Ethereum into Bitcoin in the hope the purloined funds will gather greater value and give Kim Jong-un the money for that Burger King franchise he’s had his eye on.

The saddest story of loss goes to UK crypto investor James Howells. In 2013 he had 8000 Bitcoin he had purchased for a low, low price. The only means of accessing the Bitcoin was through a private key with its crypto coding stored on his hard drive. Long story short, the hard drive ended up in a landfill in Wales. If Howells still had that key, he’d be a billionaire now. Howells wanted to excavate the entire site, but the local council demurred for environmental reasons. He then sued the council and lost. His latest plan is to buy the landfill.

From the mailbox

“I wanted to jot an email to say a very big thanks the book recommendation you gave for the book “Growing Young” by Marata Zaraska. I turned 60 in January and thought the book sounded interesting.

I purchased three copies online via Fishpond for $80.97 + $7.95 delivery as I couldn’t find a bookstore locally stocking one. It arrived ahead of schedule. I gave the other 2 copies to my cousins who have also just turned 60 this year.

After reading it I loved it that much I have purchased another 15 copies to give to other family and some of my team.

I read your column in the Sunday Mail every week and never fails to a be great read. Keep up the great work in educating and informing.”

Super numbers changing

Inflation may be the enemy, but it does one good thing for superannuation – it lifts the limits. From 1 July, you will be able to make non-concessional contributions if your fund balance is under $2 million – up from today’s $1.9 million.

The other increase is to the Transfer Balance Cap (TBC) which also rises to $2 million on 1 July. The TBC was introduced on 1 July 2017 as part of the government’s superannuation reforms, to limit the amount an individual can transfer into a tax-free retirement phase pension within their superannuation. The TBC is indexed in line with the consumer price index (CPI) and was therefore increased to $1.7 million on 1 July 2021 and $1.9 million on 1 July 2023. However, indexation is applied proportionally, meaning that individuals with existing pension accounts receive only a portion of the increase.

When the TBC was introduced, many superannuants moved $1.6 million (the limit then) into pension mode. For them, the TBC remains unchanged, but there’s no limit on how much their pension fund can grow. For instance, someone aged 65–74 with $1.6 million in a super fund earning 9% and drawing the minimum 5% pension could see their tax-free balance rise to $1.664 million.

There is complexity for three groups: those yet to start their pension, those who haven’t used their full TBC and those who have a transition-to-retirement (TTR) pension that will meet a full condition of release before 30 June.

mage by Freepik

Those who are yet to start drawing a pension need advice. A $1.9 million transfer now gives an extra five months tax-free earnings, which could be substantial if the fund performs well, and is almost a no-brainer if a big, taxable capital gain is expected before 30 June.

I’m getting many inquiries from people who have used part of their TBC and are receiving additional lump sums from an inheritance or asset sale. Most are under the wrong impression that by waiting until July they become eligible for the entire $2 million TBC. But it’s actually a complicated formula.

CASE STUDY

Jack started a pension with $1 million in January 2018, which meant he had used $1 million of his TBC. Through myGov, he discovers that his current personal TBC is $1.714 million. This means he can transfer an additional $714,000 into pension mode before 30 June. However, if he does so, he will forfeit the opportunity to access any future indexation. If he waits until after 30 June, his increased cap will be $752,000 – that’s an additional $38,000. He will need to seek professional advice to determine the best course of action for his individual circumstances.

It’s even more complex for those currently drawing a (TTR) pension.

A TTR pension is not in retirement phase and is not assessed against the TBC until a full condition of release is met. This happens automatically at age 65, or when the trustee is notified that a condition of release has been satisfied.

It’s crucial for individuals in this situation to review their circumstances before their 65th birthday. For example, if their TTR balance exceeds their available TBC space, they may need to roll the TTR back into accumulation mode to avoid exceeding the cap.

As always, professional advice is essential in navigating these decisions.

And finally

ANAGRAMS

Dormitory – Dirty Room

Evangelist – Evil’s Agent

Desperation – A Rope Ends It

The Morse Code – Here Come Dots

Slot Machines – Cash Lost in ’em

Animosity – Is No Amity

Mother-in-law – Woman Hitler

Snooze Alarms – Alas! No More Z’s

Alec Guinness – Genuine Class

Semolina – Is No Meal

The Public Art Galleries – Large Picture Halls, I Bet

A Decimal Point – I’m a Dot in Place

The Earthquakes – That Queer Shake

Eleven plus two – Twelve plus one

Contradiction – Accord not in it

A big thank you to all you good people who read my newsletter.

If you were forwarded this newsletter by a friend and you would like to subscribe, you can do so here:

For more Noel News:

You can also find the subscription box in the footer of all website pages.

I hope you have enjoyed the latest edition of Noel News.

Thanks for all your kind comments. Please continue to send feedback through; it’s always appreciated and helps us to improve the newsletter.

And don’t forget you’ll get more regular communications from me if you follow me on X – @NoelWhittaker.

Noel Whittaker