Noel News

“If you want your children to turn out well,

spend twice as much time with them,

and half as much money on them.”

ABIGAIL VAN BUREN

Welcome to our March Newsletter

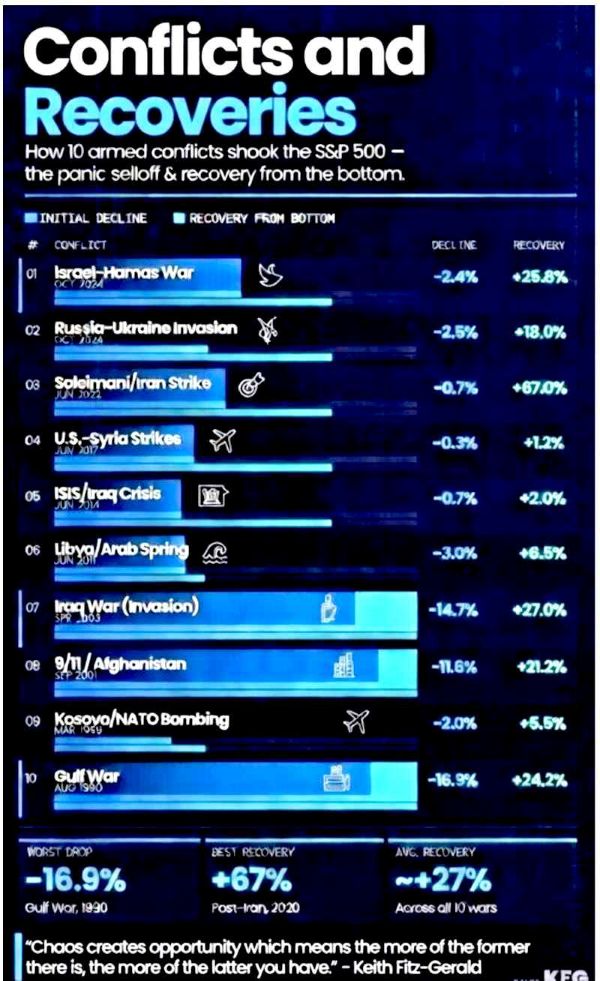

I’m writing this at a time when there is a war going on in Iran, but hopefully it won’t drag on for too long. The big question people are asking me right now is: What should I do with my shares?

The markets have never once failed to recover from a war related dip.

Let’s start by recognising that there are really two basic types of people who invest in shares:

The first are traders, who sit glued to their screens and charts and are solely focused on making a quick kill. In periods of uncertainty like this, they tend to move in and out of the market very quickly, and as a result prices can become extremely volatile. But that volatility is the price we pay for the amazing liquidity that shares offer.

The second are investors like myself, who are in it for the long term and understand that the share market will rise and fall, sometimes quite sharply, but that over time the overall trend has always been upwards. When you own a share portfolio, you’re actually a part-owner of many businesses.

And if you’re in an Australian or International managed fund, as I am, that means you own a slice of companies like BHP, Woolworths, Tesla, Visa, Amazon, Harvey Norman, JB Hi-Fi, and all the other big ones. There is no reason to think that a war in the Middle East will have much impact on these businesses in the long run.

Slow and steady wins the race.

PODCAST

Making Money

Made Simple

with Noel Whittaker

Renowned broadcaster John Deeks and I discuss all the big topics covered in this newsletter in detail each month.

Capital Gains Tax

I flagged potential changes to capital gains tax in the last newsletter, and of course now it’s all over the news with a whole range of opinions. I noticed that negative gearing has been in the headlines, and there is now talk of an attempt to tax the very wealthy. As one commentator pointed out, it seems unfair to tax an ordinary couple heavily on a capital gain they make, when a person can buy a harbourside mansion for $30 million and sell it for $70 million and make $40 million tax-free. Irrespective of what happens, I can’t see that chasing away investors is going to do anything to make homes more affordable for first home buyers.

Having said that, there’s no doubt right now that investors are surging into residential property. I guess they want to get in before any capital gains tax changes in May.

Keep in mind the committee on taxation has to lodge its final report by 14 March, which is only a couple of weeks away. Then it’s just another eight weeks until the federal budget, when all the speculation will be transformed into potential legislation. Watch this space.

Upcoming Events

Melbourne Ageing Well Expo

Fri, 20 Mar, 9:30am – Sat, 21 Mar, 4pm AEDT

The Ageing Well Expo returns to Melbourne, offering individuals and families practical tools and trusted insights to help them make informed choices for the future on their terms.

Designed to empower people to live well at every stage of life, the Expo showcases the latest innovations in health, aged care, lifestyle and wellbeing. With a wide range of products, services and resources on display, visitors will gain access to clear, practical information and expert advice to help navigate the ageing journey with confidence.

With more than 60 exhibitors, the Expo covers the full spectrum – residential care, home support, retirement living, medical services, equipment providers, and legal and financial support – providing a comprehensive picture of what it really means to age well today.

I’ll be presenting Making Money and Saving Tax in Challenging Times at the Uniting Age Well Central Stage on Friday, 20 March, from 10:15 am to 11:15 am. From 12:45 am to 1:15 pm, my colleague Rachel Lane will be talking on Making Confident Choices about Aged Care Costs.

WHEN

Friday, 20 March, 9:30am to Saturday, 21 March, 4pm

WHERE:

Melbourne Convention and Exhibition Centre

1 Convention Centre Place, South Wharf

The next stage of life

Image by Centre for Ageing Better on Unsplash

Whenever I make a speech to retirees, I always begin with one of the most basic questions people need to think about. It’s almost inevitable that at some point you – or your partner, if you’re in a couple – will need care. Is your home one where that care can be provided? That became very real for me two years ago when I broke my ankle and discovered it was impossible to live in our present home without making some modifications.

That line of thinking leads straight to the next big question. Do you expect to live in your current home for the rest of your life, perhaps with some changes along the way, or do you plan to move? And if you do move, where to?

Image by Clay Banks on Unsplash

Moving to an exotic location may sound like paradise, but I recommend renting first in the area of your choice, ideally for 12 months, but at least for six months. It gives you time to experience the environment and, just as importantly, to see what sort of social network you are realistically likely to build. It’s a simple step that can save you from making a very expensive mistake.

If you move, will your next home be an apartment, a smaller house or townhouse, or some form of retirement village accommodation? For most people, I think the most appropriate option is a retirement village. There’s a wealth of research showing that a happy and healthy retirement depends on a good diet, regular exercise, a sense of purpose, and a strong social network. A good retirement village can provide all of those.

Image by Freepik

I always tell audiences about Harry and Margaret, who retired to the Sunshine Coast. Harry kept himself busy doing casual work as a handyman, while Margaret played golf. Life was very good. But after a few years it all became a bit too much, so they moved into a retirement village in the Sunshine Coast hinterland.

Harry loved it – especially the daily happy hour, where he would sit with Margaret and five widows from the village, enjoying good conversation and a few glasses of wine. They called it Harry’s harem.

Time passed, and then life took an unexpected turn. Harry died, fairly suddenly.

But here’s the important part. If they’d been living in an apartment where they knew hardly anyone, Margaret’s world would have shrunk overnight. Instead, her life in the village carried on. The same people were there, the same routines, the same support – exactly when she needed it most.

Image by Freepik

That’s the real value of a social network, and it’s something many people underestimate the value of when they’re planning for retirement. There’s plenty more to say about retirement villages – the good, the bad and the expensive – but that’s a conversation for another column.

The next big issue for anyone planning retirement and the home for this phase of life is how to fund it. Ideally, you want to retire mortgage-free. If you’re still working, you should be using every option available to boost your super, so there’s at least enough money there to deal with any mortgage debt when you retire.

I’m often asked whether people should focus on paying off the mortgage or boosting their super.

Image by pch.vector on Freepik

Making tax-deductible contributions is usually a no-brainer, because they come from pre-tax dollars, whereas mortgage repayments are made from after-tax income. On top of that, a good super fund should be earning a higher return than the interest you’re paying on your mortgage. And remember, if you have sufficient super, you don’t necessarily need to eliminate the debt as soon as you retire – you can draw enough from super to pay the interest while the remaining super balance continues to compound.

The other critical factor is time. If you’re 60, earning $100,000 a year and have $500,000 in super, that’s all you’ll have when you retire – and you’ll still be seven years short of qualifying for the age pension. Working for five more years could lift your super balance to around $800,000. There are also strategies such as transition-to-retirement pensions, which allow you to access part of your super once you turn 60 while continuing to work, often on reduced hours.

The key point is this: the more you get into your super, and the longer you can delay drawing on it, the more you’ll have when you eventually need it.

Where you live and how you pay for it are two of the biggest issues facing any retiree. Do yourself a favour and think about the things that you, like almost everybody else, are likely to face.

“Be decisive. Right or wrong, make a decision. The road of life is paved with flat squirrels who couldn’t make a decision.”

~ Unknown

Win your relationship

From time to time I like to share what my son James is working on.

Some years ago, he reluctantly attended an event in Los Angeles and found himself seated next to Dr John Gray, author of Men Are from Mars, Women Are from Venus.

That chance conversation led to what became the most-watched episode in the history of his Win the Day podcast.

Listeners have been asking for a follow-up ever since — and James has now recorded a new conversation with Dr Gray.

In this latest episode, they explore modern relationships.

John shares:

Why understanding hormones is the key to lasting attraction

The #1 reason couples fall into a rut -and how to fix it

The truth about modern masculinity and feminine power

And how to build a relationship that gets better with time

If relationships — whether your own, your children’s, or your grandchildren’s — are an area of interest, you may find this discussion worthwhile.

Scams!!

The email stopped me in my tracks. It was a sharp reminder of just how sophisticated online scams have become. The writer explained that they had been looking for somewhere to invest and clicked on what appeared to be an online advertisement for Citibank, offering a great return. After completing an enquiry form, they were contacted by a man who introduced himself as a manager in one of the bank’s departments.

He sounded professional and knowledgeable, and had a convincing LinkedIn profile, with a Citibank job title, so the alarm bells stayed silent. By that point, the investor was seriously considering committing $500,000. Then came a moment of hesitation – a small voice saying, “Check a bit further.” That pause saved them from a very expensive mistake. The enquiry had been hijacked, the identity stolen, and the person on the phone was a scammer.

Scammers are busier than ever, and they’re getting more sophisticated by the day. What can we do to protect ourselves?

There are three simple rules that will help.

Rule one: Never accept unsolicited phone calls about investing.

Anyone who truly knew how to generate the astronomical returns promised would not be cold-calling strangers. They would be quietly getting rich themselves.

Rule two: Never go searching online if you have money to invest.

If you are looking to invest your hard-earned money, that’s the worst thing you can do. It is like swimming with the sharks. Fake sites are everywhere, and scammers are experts at making them look genuine.

Instead, get financial advice from a qualified adviser you can meet in person in their office. There is more to this than safety alone. Good advice can introduce you to strategies and opportunities you may never have heard of and help make your money work harder. Remember, good advice should save more than it costs.

Rule three: Never fill in online enquiry forms about investments.

Their sole purpose is to get you on the phone and talk you into handing over your money.

These rules may sound basic, but as so much has moved online, this is exactly how most people get caught.

This raises an obvious question: If you want to look up a well-known organisation, how do you know the website is genuine?

ASIC’s website, MoneySmart, explains what to look for. Their advice is to check the web addresses carefully, as many scam sites closely mimic trusted brands’ URLs. Be cautious with shortened links and only click them if you are already confident the source is legitimate. Watch for pages that refresh several times or bounce you through different web addresses before loading – a common warning sign. If a site claims to be from a major brand or news organisation, do a quick independent search to check if it leads to the same website.

Even when you are dealing with a reputable business, you need to watch out for the fake bank account trick. Scammers can now intercept emails between businesses and customers and change both the BSB and the account number. When you transfer money online to people you have dealt with before, usually their bank details appear automatically. But if it is a new transaction, always phone the business the invoice came from. Use a number you already have, not any contact details from the invoice – they may have been altered as well. Read out the bank details and confirm them over the phone.

Still more importantly, keep your eye on the bigger picture. The greatest financial losses are often caused by decisions that were never made – or never checked – where advice could have made all the difference.

Cases include families paying hundreds of thousands of dollars in unnecessary death tax on super because nobody understood the rules; families hit with massive legal bills because a will was wrong or out of date; and unnecessary bills for capital gains tax because no advice was sought before a contract was signed. Young people commonly lose over a million dollars by the time they retire, simply because they did not tick the right box when choosing the investment option in their super fund.

Do yourself a favour. Take your finances seriously enough to work with an adviser who can steer you through the complexities of investing and taxation. Be savvy about those who want to steal your money from you, and don’t steal it from yourself by refusing professional help.

Ebooks – guidance in your pocket.

If you want to start reading the new Ebook editions of Super Made Simple 7th Ed and Retirement Made Simple 6th ed on your computer, Kindle or phone, you can find them in the Noel Whittaker Ebooks Store.

If you have previously purchased the Super Made Simple 6th Edition Ebook or Retirement Made Simple 5th Edition Ebook, you can upgrade to the latest editions for just $3.95. Your discount will be automatically applied at checkout, or use the discount code “RMSPrevious” for the Retirement Made Simple upgrade or “SMSPrevious” for the Super Made Simple upgrade. (Note it will only work if you are a purchaser of the previous edition).

SUPER MADE SIMPLE

What’s changed in the 7th Edition?

Contribution limits, tax rules, and Centrelink thresholds don’t stand still. This edition brings everything up to date for 2026.

Latest contribution caps

Current tax rules

Updated Centrelink age & tests

New thresholds and examples

Investment performance data

Clearer explanations and examples

The 7th edition is updated with new SuperRatings performance data showing how investment choices can mean hundreds of thousands more in retirement.

Complex Topics Made Simpler

Retirement income streams

Estate planning & death benefits

Relationship breakdowns

Transition-to-retirement strategies

What’s changed in the 6th Edition?

This edition brings Retirement Made Simple fully up to date for 2026

Updated Superannuation rules & caps

Current Age Pension thresholds and tests

Latest tax treatment in retirement

Revised thresholds, figures and examples

Updated discussion of legislative risk

Clearer explanation throughout

Greater coverage of emerging retirement income products and the growing importance of flexibility as rules continue to evolve

Retirement income streams

Superannuation & pensions

Tax in retirement

Estate planning & death benefits

And finally

My wife called to tell me she saw a fox on the way to work. I asked her how she knew it was on its way to work. She hung up on me.

I went to McDonald’s today and ate a Kid’s Meal. It was good, but his mom was furious…

What’s the difference between ignorance and indifference? I don’t know and I don’t care.

My friend keeps saying, “Cheer up, man. It could be worse, you could be stuck underground in a hole full of water.” I know he means well.

I tried to come up with a carpentry pun that woodwork. I think I nailed it but nobody saw it.

I entered ten puns into a competition to see if one would win. No Pun In Ten Did.

What do you call a belt made out of hundred-dollar bills? A waist of money.

There was a big paddle sale at the boat store. It was quite an oar deal.

The invention of the shovel was a groundbreaking discovery, but the invention of the broom was the one that truly swept the nation.

A friend said she didn’t understand cloning. I told her that makes two of us.

I didn’t think orthopedic shoes would help. But I stand corrected.

I accidentally passed my wife a glue stick instead of a chapstick. She’s still not talking to me.

What do you call a melon that’s not allowed to get married? Cantelope.

I once dated a girl with a lazy eye. I always thought she was seeing someone on the side.

A big thank you to all you good people who read my newsletter.

If you were forwarded this newsletter by a friend and you would like to subscribe, you can do so here:

You can also find the subscription box in the footer of all website pages.

For more Noel News:

Download recent Noel News as a PDF

I hope you have enjoyed the latest edition of Noel News.

Thanks for all your kind comments. Please continue to send feedback through; it’s always appreciated and helps us to improve the newsletter.

And don’t forget you’ll get more regular communications from me if you follow me on X – @NoelWhittaker.

Noel Whittaker